|

| | | | | | |

| | |

| | | | | | |

| | |

| | |

| Fourth Quarter 2011 | |

| | | | | | |

| Supplemental Operating and Financial Data | |

| | | | | | |

| for the Quarter Ended December 31, 2011 | |

| | | | | | |

| Contact: | | 6110 Executive Boulevard | |

| William T. Camp | | Suite 800 | |

| Executive Vice President and | | Rockville, MD 20852 | |

| Chief Financial Officer | | (301) 984-9400 | |

| E-mail: bcamp@writ.com | | (301) 984-9610 fax | |

| | | | | | |

|

| | | | | | | | | |

| | | | | | | | | |

Company Background and Highlights | | | | | |

Fourth Quarter 2011 | | | | | |

| | | | | | | | | |

| | | | | | | | | |

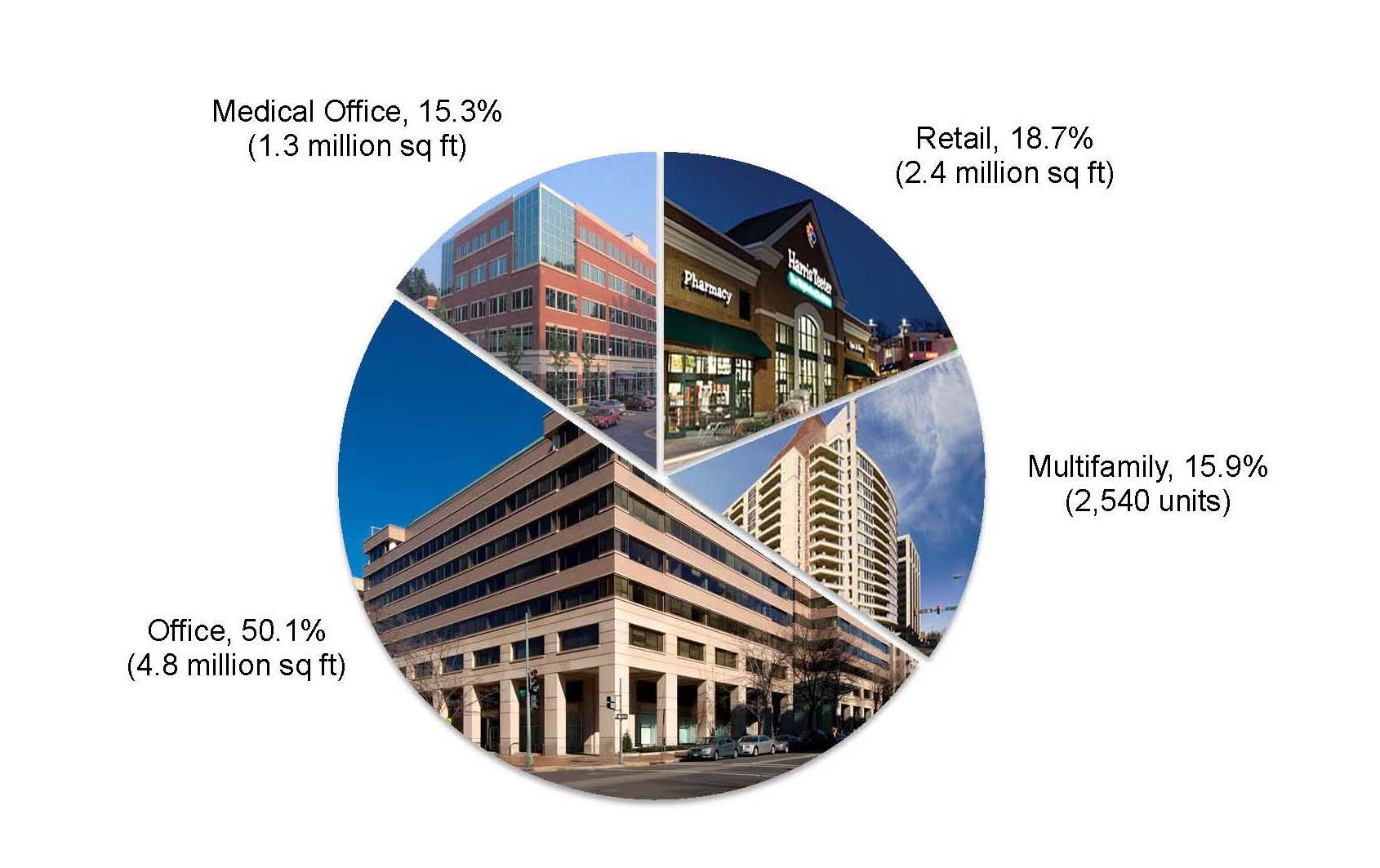

Washington Real Estate Investment Trust ("WRIT") is a self-administered, self-managed, equity real estate investment trust investing in income-producing properties in the greater Washington metro region. WRIT is diversified, as it invests in office, medical office, retail, and multifamily properties and land for development.

2011 Highlights

In 2011 WRIT acquired a record $360 million of income-producing property: 1140 Connecticut Avenue and 1227 25th Street, two office assets in downtown Washington, DC; Olney Village Center, a grocery-anchored shopping center in the heart of Olney, Maryland; Braddock Metro Center, a four-building office campus located at the Braddock Metro in Alexandria, Virginia; and John Marshall II, an office property situated on a future Metro stop in Tysons Corner, Virginia. WRIT also completed the sale of its entire industrial portfolio along with three non-strategic office assets for total proceeds of $409 million and GAAP gains of approximately $97 million. WRIT entered into two joint ventures to develop 430 multifamily units at two excellent locations in the Ballston neighborhood of Arlington, Virginia and also in Alexandria, Virginia. Construction is expected to commence on both sites in late 2012.

WRIT posted same-store GAAP rental rate growth of 2.1% in 2011 and executed 1 million square feet of commercial lease transactions.

On the capital side, WRIT replaced and expanded one of its two credit facilities, increasing its size from $262 million to $400 million with an accordion feature that allows WRIT to increase the facility to $600 million, subject to additional lender commitments. The new facility matures July 1, 2014 with a one-year extension option and bears interest at a rate of LIBOR plus a margin of 122.5 basis points based on WRIT's current credit rating.

Fourth Quarter 2011 Update

WRIT announced a joint venture with Trammell Crow Company to develop a 15-story, 270 unit high-rise apartment community in Alexandria, Virginia. The joint venture purchased the proposed development site, a one-acre parcel located at 1219 First Street in Old Town Alexandria, Virginia. The project is within walking distance of the Braddock Road Metro Station and is in close proximity to Braddock Metro Center, the 345,000 square foot office campus purchased by WRIT in September 2011. The total cost of the project is estimated to be $95 million, with a projected stabilized return on cost between 7.0% and 8.0%. WRIT is the 95% equity partner and Trammell Crow is the 5% sponsor/developer partner. Construction is projected to commence in fourth quarter 2012 and will take approximately 24 months to complete. Stabilization is estimated by first quarter 2016.

WRIT completed the final two sale transactions of its industrial portfolio disposition. The two transactions totaled $115.1 million of sales proceeds and included Northern Virginia Industrial Park II, 6100 Columbia Park Road, and Dulles Business Park.

WRIT signed commercial leases for 264,000 square feet with an average lease term of 4.8 years. The average rental rate increase on new and renewal leases was 7.9% on a GAAP basis and -4.0% on a cash basis. Commercial tenant improvement costs were $17.09 per square foot and leasing costs were $10.29 per square foot for the quarter.

As of December 31, 2011, WRIT owned a diversified portfolio of 71 properties totaling approximately 9 million square feet of commercial space and 2,540 residential units, and land held for development. These 71 properties consist of 26 office properties, 18 medical office properties, 16 retail centers and 11 multifamily properties. WRIT shares are publicly traded on the New York Stock Exchange (NYSE: WRE).

|

| | | | | | | | | |

| | | | | | | | | |

Net Operating Income Contribution by Sector* | | | |

Fourth Quarter 2011 | | | | | |

| | | | | | | | | |

| | | | | | | | | |

With investments in the office, medical office, retail and multifamily segments, WRIT is uniquely diversified. Management believes this balanced portfolio provides stability during market fluctuations in specific property types.

Net Operating Income Contribution by Sector

Certain statements in our earnings release and on our conference call are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially. Such risks, uncertainties and other factors include, but are not limited to, the potential for federal government budget reductions, changes in general and local economic and real estate market conditions, the timing and pricing of lease transactions, the effect of the current credit and financial market conditions, the availability and cost of capital, fluctuations in interest rates, tenants' financial conditions, levels of competition, the effect of government regulation, the impact of newly adopted accounting principles, and other risks and uncertainties detailed from time to time in our filings with the SEC, including our 2010 Form 10-K and third quarter 2011 Form 10-Q. We assume no obligation to update or supplement forward-looking statements that become untrue because of subsequent events.

|

| | | | |

| | | | |

Supplemental Financial and Operating Data |

Table of Contents |

December 31, 2011 |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

Schedule | | Page | |

| | | | |

Key Financial Data | | | |

| Consolidated Statements of Operations | | | |

| Consolidated Balance Sheets | | | |

| Funds From Operations and Funds Available for Distribution | | |

| Adjusted Earnings Before Interest Taxes Depreciation and Amortization (EBITDA) | | |

| | | | |

Capital Analysis | | | |

| Long-Term Debt Analysis | | | |

| Debt Covenant Compliance | | | |

| Capital Analysis | | | |

| | | | |

Portfolio Analysis | | | |

| Same-Store Portfolio Net Operating Income (NOI) Growth & Rental Rate Growth | | |

| Same-Store Portfolio Net Operating Income (NOI) Detail for the Quarter | | |

| Same-Store Portfolio Net Operating Income (NOI) Detail for the Year | | |

| Net Operating Income (NOI) by Region | | | |

| Same-Store Portfolio & Overall Physical Occupancy Levels by Sector | | |

| Same-Store Portfolio & Overall Economic Occupancy Levels by Sector | | |

Tenant Analysis | | | |

| Commercial Leasing Summary | | | |

| 10 Largest Tenants - Based on Annualized Base Rent | | |

| Industry Diversification | | | |

| Lease expirations as of December 31, 2011 | | | |

| | | | |

Growth and Strategy | | | |

| 2011 Acquisition and Disposition Summary | | | |

| | | | |

Appendix | | | |

| Schedule of Properties | | | |

| Supplemental Definitions | | | |

|

| | | | |

Consolidated Statements of Operations (In thousands, except per share data) (Unaudited)

| | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Twelve Months Ended | | Three Months Ended |

OPERATING RESULTS | 12/31/2011 | | 12/31/2010 | | 12/31/2011 | | 9/30/2011 | | 6/30/2011 | | 3/31/2011 | | 12/31/2010 |

Real estate rental revenue | $ | 289,527 |

| | $ | 258,490 |

| | $ | 76,708 |

| | $ | 71,931 |

| | $ | 71,684 |

| | $ | 69,204 |

| | $ | 65,364 |

|

Real estate expenses | (97,192 | ) | | (86,660 | ) | | (26,068 | ) | | (24,070 | ) | | (23,801 | ) | | (23,253 | ) | | (21,033 | ) |

| 192,335 |

| | 171,830 |

| | 50,640 |

| | 47,861 |

| | 47,883 |

| | 45,951 |

| | 44,331 |

|

| | | | | | | | | | | | | |

Real estate depreciation and amortization | (93,297 | ) | | (80,066 | ) | | (25,398 | ) | | (23,479 | ) | | (22,526 | ) | | (21,894 | ) | | (20,492 | ) |

Income from real estate | 99,038 |

| | 91,764 |

| | 25,242 |

| | 24,382 |

| | 25,357 |

| | 24,057 |

| | 23,839 |

|

| | | | | | | | | | | | | |

Other income | 1,144 |

| | 1,193 |

| | 258 |

| | 270 |

| | 310 |

| | 306 |

| | 318 |

|

Acquisition costs | (3,607 | ) | | (1,161 | ) | | (36 | ) | | (1,600 | ) | | (322 | ) | | (1,649 | ) | | (709 | ) |

Gain from non-disposal activities | — |

| | 7 |

| | — |

| | — |

| | — |

| | — |

| | 3 |

|

Real estate impairment | (14,526 | ) | | — |

| | (14,526 | ) | | — |

| | — |

| | — |

| | — |

|

Gain (loss) on extinguishment of debt | (976 | ) | | (9,176 | ) | | (976 | ) | | — |

| | — |

| | — |

| | (8,896 | ) |

Interest expense | (66,473 | ) | | (67,229 | ) | | (16,207 | ) | | (16,508 | ) | | (16,865 | ) | | (16,893 | ) | | (17,567 | ) |

General and administrative | (15,728 | ) | | (14,406 | ) | | (4,140 | ) | | (3,837 | ) | | (4,049 | ) | | (3,702 | ) | | (3,951 | ) |

Income (loss) from continuing operations | (1,128 | ) | | 992 |

| | (10,385 | ) | | 2,707 |

| | 4,431 |

| | 2,119 |

| | (6,963 | ) |

Discontinued operations: | | | | | | | | | | | | | |

Income from operations of properties sold or held for sale | 10,153 |

| | 14,968 |

| | 631 |

| | 3,655 |

| | 3,298 |

| | 2,569 |

| | 3,921 |

|

Income tax benefit (expense) | (1,138 | ) | | — |

| | — |

| | 35 |

| | (1,173 | ) | | — |

| | — |

|

Gain on sale of real estate | 97,491 |

| | 21,599 |

| | 40,852 |

| | 56,639 |

| | — |

| | — |

| | 13,657 |

|

Income from discontinued operations | 106,506 |

| | 36,567 |

| | 41,483 |

| | 60,329 |

| | 2,125 |

| | 2,569 |

| | 17,578 |

|

| | | | | | | | | | | | | |

Net income | 105,378 |

| | 37,559 |

| | 31,098 |

| | 63,036 |

| | 6,556 |

| | 4,688 |

| | 10,615 |

|

Less: Net income from noncontrolling interests | (494 | ) | | (133 | ) | | (409 | ) | | (28 | ) | | (34 | ) | | (23 | ) | | (24 | ) |

Net income attributable to the controlling interests | $ | 104,884 |

| | $ | 37,426 |

| | $ | 30,689 |

| | $ | 63,008 |

| | $ | 6,522 |

| | $ | 4,665 |

| | $ | 10,591 |

|

| | | | | | | | | | | | | |

Per Share Data: | | | | | | | | | | | | | |

Net income attributable to the controlling interests | $ | 1.58 |

| | $ | 0.60 |

| | $ | 0.46 |

| | $ | 0.95 |

| | $ | 0.10 |

| | $ | 0.07 |

| | $ | 0.16 |

|

| | | | | | | | | | | | | |

Fully diluted weighted average shares outstanding | 65,982 |

| | 62,264 |

| | 66,069 |

| | 66,064 |

| | 65,989 |

| | 65,907 |

| | 64,536 |

|

| | | | | | | | | | | | | |

Percentage of Revenues: | | | | | | | | | | | | | |

Real estate expenses | 33.6 | % | | 33.5 | % | | 34.0 | % | | 33.5 | % | | 33.2 | % | | 33.6 | % | | 32.2 | % |

General and administrative | 5.4 | % | | 5.6 | % | | 5.4 | % | | 5.3 | % | | 5.6 | % | | 5.3 | % | | 6.0 | % |

| | | | | | | | | | | | | |

Ratios: | | | | | | | | | | | | | |

Adjusted EBITDA / Interest expense | 2.9x |

| | 2.8x |

| | 3.0x |

| | 2.9x |

| | 3.0x |

| | 2.8x |

| | 2.7x |

|

Income (loss) from continuing operations attributable to the controlling interest/Total real estate revenue | (0.4 | )% | | 0.4 | % | | (13.5 | )% | | 3.8 | % | | 6.2 | % | | 3.1 | % | | (10.7 | )% |

Net income attributable to the controlling interest/Total real estate revenue | 36.2 | % | | 14.5 | % | | 40.0 | % | | 87.6 | % | | 9.1 | % | | 6.7 | % | | 16.2 | % |

| | | | | | | | | | | | | |

Note: Certain prior quarter amounts have been reclassified to conform to the current quarter presentation. | | |

|

| | | | |

Consolidated Balance Sheets (In thousands) (Unaudited) | | | |

|

| | | | | | | | | | | | | | | | | | | |

| 12/31/2011 | | 9/30/2011 | | 6/30/2011 | | 3/31/2011 | | 12/31/2010 |

Assets | | | | | | | | | |

Land | $ | 472,196 |

| | $ | 472,812 |

| | $ | 424,647 |

| | $ | 424,647 |

| | $ | 381,338 |

|

Income producing property | 1,934,587 |

| | 1,924,526 |

| | 1,754,493 |

| | 1,744,993 |

| | 1,670,598 |

|

| 2,406,783 |

| | 2,397,338 |

| | 2,179,140 |

| | 2,169,640 |

| | 2,051,936 |

|

Accumulated depreciation and amortization | (535,732 | ) | | (516,319 | ) | | (497,738 | ) | | (479,090 | ) | | (460,678 | ) |

Net income producing property | 1,871,051 |

| | 1,881,019 |

| | 1,681,402 |

| | 1,690,550 |

| | 1,591,258 |

|

Development in progress, including land held for development | 43,089 |

| | 39,735 |

| | 39,413 |

| | 26,263 |

| | 26,240 |

|

Total real estate held for investment, net | 1,914,140 |

| | 1,920,754 |

| | 1,720,815 |

| | 1,716,813 |

| | 1,617,498 |

|

| | | | | | | | | |

Investment in real estate held for sale, net | — |

| | 69,990 |

| | 240,437 |

| | 284,052 |

| | 286,842 |

|

Cash and cash equivalents | 12,765 |

| | 40,751 |

| | 42,886 |

| | 12,480 |

| | 78,767 |

|

Restricted cash | 19,424 |

| | 23,267 |

| | 22,311 |

| | 23,083 |

| | 20,486 |

|

Rents and other receivables, net of allowance for doubtful accounts | 53,828 |

| | 52,396 |

| | 48,472 |

| | 46,864 |

| | 44,280 |

|

Prepaid expenses and other assets | 120,601 |

| | 125,689 |

| | 99,356 |

| | 104,093 |

| | 92,040 |

|

Other assets related to properties sold or held for sale | — |

| | 3,505 |

| | 12,899 |

| | 28,827 |

| | 27,968 |

|

Total assets | $ | 2,120,758 |

| | $ | 2,236,352 |

| | $ | 2,187,176 |

| | $ | 2,216,212 |

| | $ | 2,167,881 |

|

| | | | | | | | | |

| | | | | | | | | |

Liabilities and Equity | | | | | | | | | |

Notes payable | $ | 657,470 |

| | $ | 657,378 |

| | $ | 659,934 |

| | $ | 753,692 |

| | $ | 753,587 |

|

Mortgage notes payable | 427,710 |

| | 428,909 |

| | 360,493 |

| | 361,189 |

| | 361,860 |

|

Lines of credit/short-term note payable | 99,000 |

| | 193,000 |

| | 245,000 |

| | 160,000 |

| | 100,000 |

|

Accounts payable and other liabilities | 51,145 |

| | 55,879 |

| | 54,101 |

| | 57,040 |

| | 49,138 |

|

Advance rents | 13,739 |

| | 13,393 |

| | 12,372 |

| | 11,549 |

| | 11,099 |

|

Tenant security deposits | 8,862 |

| | 8,751 |

| | 8,027 |

| | 8,024 |

| | 7,390 |

|

Other liabilities related to properties sold or held for sale | — |

| | 19,229 |

| | 24,528 |

| | 24,902 |

| | 23,949 |

|

Total Liabilities | 1,257,926 |

| | 1,376,539 |

| | 1,364,455 |

| | 1,376,396 |

| | 1,307,023 |

|

| | | | | | | | | |

Equity | | | | | | | | | |

Shares of beneficial interest, $0.01 par value; 100,000 shares authorized | 662 |

| | 661 |

| | 661 |

| | 660 |

| | 659 |

|

Additional paid-in capital | 1,138,478 |

| | 1,136,240 |

| | 1,133,823 |

| | 1,130,297 |

| | 1,127,825 |

|

Distributions in excess of net income | (280,096 | ) | | (281,930 | ) | | (316,134 | ) | | (293,860 | ) | | (269,935 | ) |

Accumulated other comprehensive income (loss) | — |

| | (160 | ) | | (636 | ) | | (1,057 | ) | | (1,469 | ) |

Total shareholders' equity | 859,044 |

| | 854,811 |

| | 817,714 |

| | 836,040 |

| | 857,080 |

|

Noncontrolling interests in subsidiaries | 3,788 |

| | 5,002 |

| | 5,007 |

| | 3,776 |

| | 3,778 |

|

Total equity | 862,832 |

| | 859,813 |

| | 822,721 |

| | 839,816 |

| | 860,858 |

|

Total liabilities and equity | $ | 2,120,758 |

| | $ | 2,236,352 |

| | $ | 2,187,176 |

| | $ | 2,216,212 |

| | $ | 2,167,881 |

|

| | | | | | | | | |

Total Debt / Total Market Capitalization | 0.40 | :1 | | 0.41 | :1 | | 0.37 | :1 | | 0.39 | :1 | | 0.38 | :1 |

|

| | | | |

Funds from Operations and Funds Available for Distribution (In thousands, except per share data) (Unaudited)

| | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Twelve Months Ended | | Three Months Ended |

| 12/31/2011 | | 12/31/2010 | | 12/31/2011 | | 9/30/2011 | | 6/30/2011 | | 3/31/2011 | | 12/31/2010 |

Funds from operations(1) | | | | | | | | | | | | | |

Net income attributable to the controlling interests | $ | 104,884 |

| | $ | 37,426 |

| | $ | 30,689 |

| | $ | 63,008 |

| | $ | 6,522 |

| | $ | 4,665 |

| | $ | 10,591 |

|

Real estate depreciation and amortization | 93,297 |

| | 80,066 |

| | 25,398 |

| | 23,479 |

| | 22,526 |

| | 21,894 |

| | 20,492 |

|

Gain from non-disposal activities | — |

| | (7 | ) | | — |

| | — |

| | — |

| | — |

| | (3 | ) |

Discontinued operations: | | | | | | | | | | | | | |

Gain on sale of real estate | (97,091 | ) | | (21,599 | ) | | (40,452 | ) | | (56,639 | ) | | — |

| | — |

| | (13,657 | ) |

Income tax expense (benefit) | 1,138 |

| | — |

| | — |

| | (35 | ) | | 1,173 |

| | — |

| | — |

|

Real estate impairment | 599 |

| | — |

| | — |

| | — |

| | — |

| | 599 |

| | — |

|

Real estate depreciation and amortization | 7,231 |

| | 15,680 |

| | — |

| | 943 |

| | 2,933 |

| | 3,355 |

| | 3,699 |

|

Funds from operations (FFO) | $ | 110,058 |

| | $ | 111,566 |

| | $ | 15,635 |

| | $ | 30,756 |

| | $ | 33,154 |

| | $ | 30,513 |

| | $ | 21,122 |

|

Loss (gain) on extinguishment of debt | 976 |

| | 9,176 |

| | 976 |

| | — |

| | — |

| | — |

| | 8,896 |

|

Real estate impairment | 14,526 |

| | — |

| | 14,526 |

| | — |

| | — |

| | — |

| | — |

|

Acquisition costs | 3,607 |

| | 1,161 |

| | 36 |

| | 1,600 |

| | 322 |

| | 1,649 |

| | 709 |

|

Core FFO (1) | $ | 129,167 |

| | $ | 121,903 |

| | $ | 31,173 |

| | $ | 32,356 |

| | $ | 33,476 |

| | $ | 32,162 |

| | $ | 30,727 |

|

| | | | | | | | | | | | | |

Allocation to participating securities(2) | (712 | ) | | (144 | ) | | (186 | ) | | (385 | ) | | (38 | ) | | (46 | ) | | (47 | ) |

| | | | | | | | | | | | | |

FFO per share - basic | $ | 1.66 |

| | $ | 1.79 |

| | $ | 0.23 |

| | $ | 0.46 |

| | $ | 0.50 |

| | $ | 0.46 |

| | $ | 0.33 |

|

FFO per share - fully diluted | $ | 1.66 |

| | $ | 1.79 |

| | $ | 0.23 |

| | $ | 0.46 |

| | $ | 0.50 |

| | $ | 0.46 |

| | $ | 0.33 |

|

| | | | | | | | | | | | | |

Core FFO per share - fully diluted | $ | 1.95 |

| | $ | 1.96 |

| | $ | 0.47 |

| | $ | 0.48 |

| | $ | 0.51 |

| | $ | 0.49 |

| | $ | 0.48 |

|

| | | | | | | | | | | | | |

Funds available for distribution(1) | | | | | | | | | | | | | |

FFO | $ | 110,058 |

| | $ | 111,566 |

| | $ | 15,635 |

| | $ | 30,756 |

| | $ | 33,154 |

| | $ | 30,513 |

| | $ | 21,122 |

|

Non-cash (gain)/loss on extinguishment of debt | — |

| | 3,202 |

| | — |

| | — |

| | — |

| | — |

| | 2,922 |

|

Tenant improvements | (11,889 | ) | | (13,579 | ) | | (5,100 | ) | | (2,469 | ) | | (1,950 | ) | | (2,370 | ) | | (6,373 | ) |

Leasing commissions and incentives | (8,692 | ) | | (9,511 | ) | | (1,485 | ) | | (3,859 | ) | | (1,116 | ) | | (2,232 | ) | | (2,089 | ) |

Recurring capital improvements | (7,537 | ) | | (5,938 | ) | | (1,626 | ) | | (2,148 | ) | | (3,072 | ) | | (691 | ) | | (1,698 | ) |

Straight-line rent, net | (2,734 | ) | | (3,470 | ) | | (776 | ) | | (715 | ) | | (586 | ) | | (657 | ) | | (951 | ) |

Non-cash fair value interest expense | 462 |

| | 2,664 |

| | (53 | ) | | 145 |

| | 191 |

| | 179 |

| | 345 |

|

Non-real estate depreciation and amortization | 3,733 |

| | 3,969 |

| | 845 |

| | 1,126 |

| | 888 |

| | 874 |

| | 889 |

|

Amortization of lease intangibles, net | (1,052 | ) | | (1,817 | ) | | (32 | ) | | (329 | ) | | (413 | ) | | (278 | ) | | (437 | ) |

Amortization and expensing of restricted share and unit compensation | 5,580 |

| | 5,852 |

| | 1,459 |

| | 1,376 |

| | 1,488 |

| | 1,257 |

| | 1,553 |

|

Funds available for distribution (FAD) | $ | 87,929 |

| | $ | 92,938 |

| | $ | 8,867 |

| | $ | 23,883 |

| | $ | 28,584 |

| | $ | 26,595 |

| | $ | 15,283 |

|

Cash loss (gain) on extinguishment of debt | 976 |

| | 5,974 |

| | 976 |

| | — |

| | — |

| | — |

| | 5,974 |

|

Real estate impairment | 14,526 |

| | — |

| | 14,526 |

| | — |

| | — |

| | — |

| | — |

|

Acquisition costs | 3,607 |

| | 1,161 |

| | 36 |

| | 1,600 |

| | 322 |

| | 1,649 |

| | 709 |

|

Core FAD (1) | $ | 107,038 |

| | $ | 100,073 |

| | $ | 24,405 |

| | $ | 25,483 |

| | $ | 28,906 |

| | $ | 28,244 |

| | $ | 21,966 |

|

| | | | | | | | | | | | | |

Allocation to participating securities(2) | (712 | ) | | (144 | ) | | (186 | ) | | (385 | ) | | (38 | ) | | (46 | ) | | (47 | ) |

| | | | | | | | | | | | | |

FAD per share - basic | $ | 1.32 |

| | $ | 1.49 |

| | $ | 0.13 |

| | $ | 0.36 |

| | $ | 0.43 |

| | $ | 0.40 |

| | $ | 0.24 |

|

FAD per share - fully diluted | $ | 1.32 |

| | $ | 1.49 |

| | $ | 0.13 |

| | $ | 0.36 |

| | $ | 0.43 |

| | $ | 0.40 |

| | $ | 0.24 |

|

| | | | | | | | | | | | | |

Core FAD per share - fully diluted | $ | 1.61 |

| | $ | 1.60 |

| | $ | 0.37 |

| | $ | 0.38 |

| | $ | 0.44 |

| | $ | 0.43 |

| | $ | 0.34 |

|

| | | | | | | | | | | | | |

Common dividend per share | $ | 1.7350 |

| | $ | 1.7313 |

| | $ | 0.4338 |

| | $ | 0.4338 |

| | $ | 0.4338 |

| | $ | 0.4338 |

| | $ | 0.4338 |

|

| | | | | | | | | | | | | |

Average shares - basic | 65,982 |

| | 62,140 |

| | 66,069 |

| | 66,017 |

| | 65,954 |

| | 65,885 |

| | 64,536 |

|

Average shares - fully diluted | 65,982 |

| | 62,264 |

| | 66,069 |

| | 66,064 |

| | 65,989 |

| | 65,907 |

| | 64,536 |

|

(1) See "Supplemental Definitions" on page 28 of this supplemental for the definitions of FFO, Core FFO, FAD and Core FAD.

(2) Adjustment to the numerators for FFO, Core FFO, FAD and Core FAD per share calculations when applying the two-class method for calculating EPS.

|

| | | | |

Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) (In thousands) (Unaudited) | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Twelve Months Ended | | Three Months Ended |

| 12/31/2011 | | 12/31/2010 | | 12/31/2011 | | 9/30/2011 | | 6/30/2011 | | 3/31/2011 | | 12/31/2010 |

Adjusted EBITDA(1) | | | | | | | | | | | | | |

| | | | | | | | | | | | | |

Net income attributable to the controlling interests | $ | 104,884 |

| | $ | 37,426 |

| | $ | 30,689 |

| | $ | 63,008 |

| | $ | 6,522 |

| | $ | 4,665 |

| | $ | 10,591 |

|

Add: | | | | | | | | | | | | | |

Interest expense, including discontinued operations | 66,947 |

| | 68,979 |

| | 15,985 |

| | 16,739 |

| | 17,097 |

| | 17,126 |

| | 17,801 |

|

Real estate depreciation and amortization, including discontinued operations | 100,528 |

| | 95,746 |

| | 25,398 |

| | 24,422 |

| | 25,459 |

| | 25,249 |

| | 24,191 |

|

Income tax expense (benefit) | 1,146 |

| | — |

| | — |

| | (27 | ) | | 1,173 |

| | — |

| | — |

|

Real estate impairment | 15,125 |

| | — |

| | 14,526 |

| | — |

| | — |

| | 599 |

| | — |

|

Non-real estate depreciation | 1,001 |

| | 1,102 |

| | 242 |

| | 243 |

| | 248 |

| | 268 |

| | 279 |

|

Less: | | | | | | | | | | | | | |

Gain on sale of real estate | (97,091 | ) | | (21,599 | ) | | (40,452 | ) | | (56,639 | ) | | — |

| | — |

| | (13,657 | ) |

Loss (gain) on extinguishment of debt | 976 |

| | 9,176 |

| | 976 |

| | — |

| | — |

| | — |

| | 8,896 |

|

Gain from non-disposal activities | — |

| | (7 | ) | | — |

| | — |

| | — |

| | — |

| | (3 | ) |

| | | | | | | | | | | | | |

Adjusted EBITDA | $ | 193,516 |

| | $ | 190,823 |

| | $ | 47,364 |

| | $ | 47,746 |

| | $ | 50,499 |

| | $ | 47,907 |

| | $ | 48,098 |

|

| | | | | | | | | | | | | |

(1) Adjusted EBITDA is earnings before interest expense, taxes, depreciation, amortization, gain on sale of real estate, gain/loss on extinguishment of debt and gain from non-disposal activities. We consider Adjusted EBITDA to be an appropriate supplemental performance measure because it permits investors to view income from operations without the effect of depreciation, the cost of debt or non-operating gains and losses. Adjusted EBITDA is a non-GAAP measure. |

|

| | | | |

Long Term Debt Analysis (In thousands, except per share data) | | |

|

| | | | | | | | | | | | | | | | | | | |

| 12/31/2011 | | 9/30/2011 | | 6/30/2011 | | 3/31/2011 | | 12/31/2010 |

Balances Outstanding | | | | | | | | | |

| | | | | | | | | |

Secured | | | | | | | | | |

Conventional fixed rate | $ | 427,710 |

| | $ | 446,715 |

| | $ | 378,469 |

| | $ | 379,333 |

| | $ | 380,171 |

|

Secured total | 427,710 |

| | 446,715 |

| | 378,469 |

| | 379,333 |

| | 380,171 |

|

Unsecured | | | | | | | | | |

Fixed rate bonds and notes | 657,470 |

| | 657,378 |

| | 659,934 |

| | 753,692 |

| | 753,587 |

|

Credit facility | 99,000 |

| | 193,000 |

| | 245,000 |

| | 160,000 |

| | 100,000 |

|

Unsecured total | 756,470 |

| | 850,378 |

| | 904,934 |

| | 913,692 |

| | 853,587 |

|

Total | $ | 1,184,180 |

| | $ | 1,297,093 |

| | $ | 1,283,403 |

| | $ | 1,293,025 |

| | $ | 1,233,758 |

|

| | | | | | | | | |

Average Interest Rates | | | | | | | | | |

| | | | | | | | | |

Secured | | | | | | | | | |

Conventional fixed rate | 5.9 | % | | 5.9 | % | | 5.9 | % | | 5.9 | % | | 5.9 | % |

Secured total | 5.9 | % | | 5.9 | % | | 5.9 | % | | 5.9 | % | | 5.9 | % |

Unsecured | | | | | | | | | |

Fixed rate bonds | 5.4 | % | | 5.4 | % | | 5.4 | % | | 5.4 | % | | 5.4 | % |

Credit facilities | 0.9 | % | | 2.1 | % | | 1.4 | % | | 1.8 | % | | 2.5 | % |

Unsecured total | 4.8 | % | | 4.6 | % | | 4.3 | % | | 4.8 | % | | 5.1 | % |

Average | 5.2 | % | | 5.1 | % | | 4.8 | % | | 5.1 | % | | 5.4 | % |

Note: The current balances outstanding of the secured and unsecured fixed rate bonds and notes are shown net of discounts/premiums in the amount of $4.5 million and $2.5 million, respectively.

|

| | | | |

Long Term Debt Analysis (In thousands, except per share amounts) | | | |

|

| | | | | | | | | | | | | | | | | | |

| | Future Maturities of Debt |

Year | | Secured Debt | | Unsecured Debt | | Credit Facilities | | Total Debt | | Average Interest Rate |

2012 | | $ | 27,000 |

| | $ | 50,000 |

| | 74,000 |

| | $ | 151,000 |

| | 3.0% |

2013 | | 87,580 |

| | 60,000 |

| | — |

| | 147,580 |

| | 5.4% |

2014 | | 3,724 |

| | 100,000 |

| | 25,000 |

| | 128,724 |

| | 4.6% |

2015 | | 22,390 |

| | 150,000 |

| | — |

| | 172,390 |

| | 5.4% |

2016 | | 134,943 |

| | — |

| | — |

| | 134,943 |

| | 5.7% |

2017 | | 104,953 |

| | — |

| | — |

| | 104,953 |

| | 7.2% |

2018 | | 3,277 |

| | — |

| | — |

| | 3,277 |

| | 5.1% |

2019 | | 34,060 |

| | — |

| | — |

| | 34,060 |

| | 5.3% |

2020 | | 2,818 |

| | 250,000 |

| | — |

| | 252,818 |

| | 5.1% |

2021 | | 2,997 |

| | — |

| | — |

| | 2,997 |

| | 5.1% |

2022 | | 3,187 |

| | — |

| | — |

| | 3,187 |

| | 5.1% |

Thereafter | | 5,256 |

| | 50,000 |

| | — |

| | 55,256 |

| | 7.2% |

Total maturities | | $ | 432,185 |

| | $ | 660,000 |

| | $ | 99,000 |

| | $ | 1,191,185 |

| | 5.2% |

Weighted average maturity = 5.0 years

|

| | | | | | | | | | | | | | | | |

| Unsecured Notes Payable | | Unsecured Line of Credit #1

($75.0 million) | | Unsecured Line of Credit #2

($400.0 million) |

| Quarter Ended December 31, 2011 | | Covenant | | Quarter Ended December 31, 2011 | | Covenant | | Quarter Ended December 31, 2011 | | Covenant |

| | | | | | | | | | | |

% of Total Indebtedness to Total Assets(1) | 41.0 | % | | ≤ 65.0% | | N/A |

| | N/A | | N/A |

| | N/A |

Ratio of Income Available for Debt Service to Annual Debt Service | 3.1 |

| | ≥ 1.5 | | N/A |

| | N/A | | N/A |

| | N/A |

% of Secured Indebtedness to Total Assets(1) | 14.8 | % | | ≤ 40.0% | | N/A |

| | N/A | | N/A |

| | N/A |

Ratio of Total Unencumbered Assets(2) to Total Unsecured Indebtedness | 2.8 |

| | ≥ 1.5 | | N/A |

| | N/A | | N/A |

| | N/A |

Tangible Net Worth(3) | N/A |

| | N/A | |

| $1.1 billion |

| | ≥ $808.6 million | |

| $843.0 million |

| | ≥ $671.9 million |

% of Total Liabilities to Gross Asset Value(5) | N/A |

| | N/A | | 50.3 | % | | ≤ 60.0% | | 48.7 | % | | ≤ 60.0% |

% of Secured Indebtedness to Gross Asset Value(5) | N/A |

| | N/A | | 17.1 | % | | ≤ 35.0% | | 16.6 | % | | ≤ 35.0% |

Ratio of EBITDA(4) to Fixed Charges(6) | N/A |

| | N/A | | 2.58 |

| | ≥ 1.75 | | 2.58 |

| | ≥ 1.50 |

Ratio of Unencumbered Pool Value(8) to Unsecured Indebtedness | N/A |

| | N/A | | 2.47 |

| | ≥ 1.67 | | 2.48 |

| | ≥ 1.67 |

Ratio of Unencumbered Net Operating Income to Unsecured Interest Expense | N/A |

| | N/A | | N/A |

| | N/A | | 3.56 |

| | ≥ 2.00 |

% of Development in Progress to Gross Asset Value(5) | N/A |

| | N/A | | 1.7 | % | | ≤ 30.0% | | N/A |

| | N/A |

% of Non-Wholly Owned Assets(7) to Gross Asset Value(5) | N/A |

| | N/A | | 0.8 | % | | ≤ 15.0% | | N/A |

| | N/A |

Ratio of Investments(9) to Gross Asset Value(5) | N/A |

| | N/A | | N/A |

| | N/A | | 1.7 | % | | ≤ 15.0% |

| | | | | | | | | | | |

(1) Total Assets is calculated by applying a capitalization rate of 7.50% to the EBITDA(4) from the last four consecutive quarters, excluding EBITDA from acquired, disposed, and non-stabilized development properties. |

(2) Total Unencumbered Assets is calculated by applying a capitalization rate of 7.50% to the EBITDA(4) from unencumbered properties from the last four consecutive quarters, excluding EBITDA from acquired, disposed, and non-stabilized development properties. |

(3) Tangible Net Worth is defined as shareholders equity less accumulated depreciation at the commitment start date plus current accumulated depreciation. |

(4) EBITDA is defined in our debt covenants as earnings before minority interests, depreciation, amortization, interest expense, income tax expense, and extraordinary and nonrecurring gains and losses. |

(5) Gross Asset Value is calculated by applying a capitalization rate to the annualized EBITDA(4) from the most recently ended quarter, excluding EBITDA from disposed properties and current quarter acquisitions. To this amount, the purchase price of current quarter acquisitions, cash and cash equivalents and development in progress is added. |

(6) Fixed Charges consist of interest expense, principal payments, ground lease payments and replacement reserve payments. |

(7) Non-Wholly Owned Assets is calculated by applying a capitalization rate of 7.50% to the EBITDA(4) from properties subject to a joint operating agreement (i.e. NVIP I&II). We add to this amount the development in progress subject to a joint operating agreement (i.e. 4661 Kenmore Avenue). |

(8) Unencumbered Pool Value is calculated by applying a capitalization rate of 7.75% to the net operating income from unencumbered properties owned for the entire quarter. To this we add the purchase price of unencumbered acquisitions during the current quarter and, for Unsecured Line of Credit #1 only, development in progress. |

(9) Investments is defined as development in progress, including land held for development, plus budgeted development costs upon commencement of construction, if any. |

|

| | | | |

Capital Analysis (In thousands, except per share amounts) | | |

|

| | | | | | | | | | | | | | | | | | | |

| 12/31/2011 | | 9/30/2011 | | 6/30/2011 | | 3/31/2011 | | 12/31/2010 |

Market Data | | | | | | | | | |

| | | | | | | | | |

Shares Outstanding | 66,265 |

| | 66,066 |

| | 66,017 |

| | 65,941 |

| | 65,870 |

|

Market Price per Share | $ | 27.35 |

| | $ | 28.18 |

| | $ | 32.52 |

| | $ | 31.09 |

| | $ | 30.99 |

|

Equity Market Capitalization | $ | 1,812,348 |

| | $ | 1,861,740 |

| | $ | 2,146,873 |

| | $ | 2,050,106 |

| | $ | 2,041,311 |

|

| | | | | | | | | |

Total Debt | $ | 1,184,180 |

| | $ | 1,297,093 |

| | $ | 1,283,403 |

| | $ | 1,293,025 |

| | $ | 1,233,758 |

|

Total Market Capitalization | $ | 2,996,528 |

| | $ | 3,158,833 |

| | $ | 3,430,276 |

| | $ | 3,343,131 |

| | $ | 3,275,069 |

|

| | | | | | | | | |

Total Debt to Market Capitalization | 0.40 | :1 | | 0.41 | :1 | | 0.37 | :1 | | 0.39 | :1 | | 0.38 | :1 |

| | | | | | | | | |

Earnings to Fixed Charges(1) | 0.3x |

| | 1.1x |

| | 1.3x |

| | 1.1x |

| | 0.6x |

|

Debt Service Coverage Ratio(2) | 2.7x |

| | 2.7x |

| | 2.8x |

| | 2.6x |

| | 2.5x |

|

| | | | | | | | | |

Dividend Data | | | | | | | | | |

| | | | | | | | | |

Total Dividends Paid | $ | 28,669 |

| | $ | 28,641 |

| | $ | 28,621 |

| | $ | 28,587 |

| | $ | 28,438 |

|

Common Dividend per Share | $ | 0.43 |

| | $ | 0.43 |

| | $ | 0.43 |

| | $ | 0.43 |

| | $ | 0.43 |

|

Payout Ratio (Core FFO per share basis) | 92.3 | % | | 90.4 | % | | 85.0 | % | | 88.5 | % | | 90.4 | % |

Payout Ratio (Core FAD per share basis) | 117.2 | % | | 114.1 | % | | 98.6 | % | | 100.9 | % | | 127.6 | % |

Payout Ratio (FAD per share basis) | 333.7 | % | | 120.5 | % | | 100.9 | % | | 108.4 | % | | 180.7 | % |

(1) The ratio of earnings to fixed charges is computed by dividing earnings by fixed charges. For this purpose, earnings consist of income from continuing operations attributable to the controlling interests plus fixed charges, less capitalized interest. Fixed charges consist of interest expense, including amortized costs of debt issuance, plus interest costs capitalized.

(2) Debt service coverage ratio is computed by dividing Adjusted EBITDA (see page 7) by interest expense and principal amortization.

|

| | | | |

Same-Store Portfolio Net Operating Income (NOI) Growth & Rental Rate Growth 2011 vs. 2010 | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended December 31, (1) | | Twelve Months Ended December 31, (2) |

| | 2011 | | 2010 | | % Change | | Rental Rate Growth | | 2011 | | 2010 | | % Change | | Rental Rate Growth |

| | | | | | | | | | | | | | | | |

Cash Basis: | | | | | | | | | | | | | | | | |

Multifamily | | $ | 7,838 |

| | $ | 7,386 |

| | 6.1 | % | | 4.6 | % | | $ | 30,464 |

| | $ | 28,550 |

| | 6.7 | % | | 4.0 | % |

Office Buildings | | 20,209 |

| | 20,006 |

| | 1.0 | % | | 1.9 | % | | 75,398 |

| | 74,157 |

| | 1.7 | % | | 2.1 | % |

Medical Office Buildings | | 7,483 |

| | 7,643 |

| | (2.1 | )% | | 3.1 | % | | 30,022 |

| | 29,924 |

| | 0.3 | % | | 3.2 | % |

Retail Centers | | 7,080 |

| | 7,353 |

| | (3.7 | )% | | 2.7 | % | | 28,716 |

| | 29,808 |

| | (3.7 | )% | | 1.5 | % |

Overall Same-Store Portfolio | | $ | 42,610 |

| | $ | 42,388 |

| | 0.5 | % | | 2.7 | % | | $ | 164,600 |

| | $ | 162,439 |

| | 1.3 | % | | 2.6 | % |

| | | | | | | | | | | | | | | | |

GAAP Basis: | | | | | | | | | | | | | | | | |

Multifamily | | $ | 8,033 |

| | $ | 7,589 |

| | 5.9 | % | | 4.5 | % | | $ | 31,262 |

| | $ | 29,356 |

| | 6.5 | % | | 4.0 | % |

Office Buildings | | 20,631 |

| | 20,930 |

| | (1.4 | )% | | 0.7 | % | | 77,187 |

| | 77,818 |

| | (0.8 | )% | | 1.0 | % |

Medical Office Buildings | | 7,707 |

| | 7,877 |

| | (2.2 | )% | | 2.9 | % | | 30,983 |

| | 30,744 |

| | 0.8 | % | | 3.4 | % |

Retail Centers | | 6,953 |

| | 7,507 |

| | (7.4 | )% | | 2.2 | % | | 28,849 |

| | 30,196 |

| | (4.5 | )% | | 1.5 | % |

Overall Same-Store Portfolio | | $ | 43,324 |

| | $ | 43,903 |

| | (1.3 | )% | | 2.0 | % | | $ | 168,281 |

| | $ | 168,114 |

| | 0.1 | % | | 2.1 | % |

(1) Non same-store properties were:

Acquisitions:

Office - 1140 Connecticut Avenue, 1227 25th Street, Braddock Metro Center and John Marshall II.

Retail - Gateway Overlook, Olney Village Center.

Medical Office - Lansdowne Medical Office Building.

Held for sale and sold properties:

Office - Dulles Station, Phase I.

Industrial/Office - Industrial Portfolio (see Supplemental Definitions for list of properties).

(2) Non same-store properties were:

Acquisitions:

Office - Quantico Corporate Center, 1140 Connecticut Avenue, 1227 25th Street, Braddock Metro Center and John Marshall II.

Retail - Gateway Overlook, Olney Village Center.

Medical Office - Lansdowne Medical Office Building.

Held for sale and sold properties:

Office - Parklawn Plaza, Lexington, Saratoga, Ridges, and Dulles Station, Phase I.

Industrial/Office - Charleston, Ammendale I & II, Amvax, and the Industrial Portfolio (see Supplemental Definitions for list of properties).

|

| | | | |

Same-Store Portfolio Net Operating Income (NOI) Detail (In thousands) | | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended December 31, 2011 |

| Multifamily | | Office | | Medical Office | | Retail | | Industrial/Flex | | Corporate and Other | | Total |

Real estate rental revenue | | | | | | | | | | | | | |

Same-store portfolio | $ | 12,906 |

| | $ | 31,111 |

| | $ | 11,057 |

| | $ | 10,218 |

| | $ | — |

| | — |

| | $ | 65,292 |

|

Non same-store - acquired and in development(1) | — |

| | 7,898 |

| | 199 |

| | 3,319 |

| | — |

| | — |

| | 11,416 |

|

Total | 12,906 |

| | 39,009 |

| | 11,256 |

| | 13,537 |

| | — |

| | — |

| | 76,708 |

|

| | | | | | | | | | | | | |

Real estate expenses | | | | | | | | | | | | | |

Same-store portfolio | 4,873 |

| | 10,480 |

| | 3,350 |

| | 3,265 |

| | — |

| | — |

| | 21,968 |

|

Non same-store - acquired and in development(1) | — |

| | 3,174 |

| | 146 |

| | 780 |

| | — |

| | — |

| | 4,100 |

|

Total | 4,873 |

| | 13,654 |

| | 3,496 |

| | 4,045 |

| | — |

| | — |

| | 26,068 |

|

| | | | | | | | | | | | | |

Net Operating Income (NOI) | | | | | | | | | | | | | |

Same-store portfolio | 8,033 |

| | 20,631 |

| | 7,707 |

| | 6,953 |

| | — |

| | — |

| | 43,324 |

|

Non same-store - acquired and in development(1) | — |

| | 4,724 |

| | 53 |

| | 2,539 |

| | — |

| | — |

| | 7,316 |

|

Total | $ | 8,033 |

| | $ | 25,355 |

| | $ | 7,760 |

| | $ | 9,492 |

| | $ | — |

| | — |

| | $ | 50,640 |

|

| | | | | | | | | | | | | |

Same-store portfolio NOI GAAP basis (from above) | $ | 8,033 |

| | $ | 20,631 |

| | $ | 7,707 |

| | $ | 6,953 |

| | $ | — |

| | — |

| | $ | 43,324 |

|

Straight-line revenue, net for same-store properties | (3 | ) | | (387 | ) | | (145 | ) | | 129 |

| | — |

| | — |

| | (406 | ) |

FAS 141 Min Rent | (192 | ) | | (155 | ) | | (89 | ) | | (78 | ) | | — |

| | — |

| | (514 | ) |

Amortization of lease intangibles for same-store properties | — |

| | 120 |

| | 10 |

| | 76 |

| | — |

| | — |

| | 206 |

|

Same-store portfolio NOI, cash basis | $ | 7,838 |

| | $ | 20,209 |

| | $ | 7,483 |

| | $ | 7,080 |

| | $ | — |

| | — |

| | $ | 42,610 |

|

| | | | | | | | | | | | | |

Reconciliation of NOI to net income | | | | | | | | | | | | | |

Total NOI | $ | 8,033 |

| | $ | 25,355 |

| | $ | 7,760 |

| | $ | 9,492 |

| | $ | — |

| | — |

| | $ | 50,640 |

|

Other income | — |

| | — |

| | — |

| | — |

| | — |

| | 258 |

| | 258 |

|

Acquisition costs | — |

| | — |

| | — |

| | — |

| | — |

| | (36 | ) | | (36 | ) |

Interest expense | (1,717 | ) | | (3,077 | ) | | (1,188 | ) | | (611 | ) | | — |

| | (9,614 | ) | | (16,207 | ) |

Depreciation and amortization | (3,175 | ) | | (14,611 | ) | | (3,856 | ) | | (3,539 | ) | | — |

| | (217 | ) | | (25,398 | ) |

General and administrative | — |

| | — |

| | — |

| | — |

| | — |

| | (4,140 | ) | | (4,140 | ) |

Real estate impairment | — |

| | — |

| | — |

| | — |

| | — |

| | (14,526 | ) | | (14,526 | ) |

Loss of Extinguishment of debt | — |

| | — |

| | — |

| | — |

| | — |

| | (976 | ) | | (976 | ) |

Gain on non disposal | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

|

Discontinued operations(2) | — |

| | 10 |

| | — |

| | — |

| | 621 |

| | — |

| | 631 |

|

Income tax benefit (expense) | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

|

Gain on sale of real estate | — |

| | — |

| | — |

| | — |

| | — |

| | 40,852 |

| | 40,852 |

|

Net Income | 3,141 |

| | 7,677 |

| | 2,716 |

| | 5,342 |

| | 621 |

| | 11,601 |

| | 31,098 |

|

Net income attribuatble to noncontrolling interests | — |

| | — |

| | — |

| | — |

| | — |

| | (409 | ) | | (409 | ) |

Net income attributable to the controlling interests | $ | 3,141 |

| | $ | 7,677 |

| | $ | 2,716 |

| | $ | 5,342 |

| | $ | 621 |

| | $ | 11,192 |

| | $ | 30,689 |

|

(1) Non same-store properties were:

Acquisitions:

Office - 1140 Connecticut Avenue, 1227 25th Street, Braddock Metro Center and John Marshall II.

Retail - Gateway Overlook, Olney Village Center.

Medical Office - Lansdowne Medical Office Building.

(2) Discontinued operations included the following held for sale and sold properties:

Office - Dulles Station, Phase I and The Ridges

Industrial/Office - Ammendale I & II, Amvax and Industrial Portfolio (see Supplemental Definitions for list of properties).

|

| | | | |

Same-Store Net Operating Income (NOI) Detail (In thousands) | | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended December 31, 2010 |

| Multifamily | | Office | | Medical Office | | Retail | | Industrial/Flex | | Corporate and Other | | Total |

Real estate rental revenue | | | | | | | | | | | | | |

Same-store portfolio | $ | 12,407 |

| | $ | 31,187 |

| | $ | 11,279 |

| | $ | 9,810 |

| | $ | — |

| | — |

| | $ | 64,683 |

|

Non same-store - acquired and in development(1) | — |

| | — |

| | 54 |

| | 627 |

| | — |

| | — |

| | 681 |

|

Total | 12,407 |

| | 31,187 |

| | 11,333 |

| | 10,437 |

| | — |

| | — |

| | 65,364 |

|

| | | | | | | | | | | | | |

Real estate expenses | | | | | | | | | | | | | |

Same-store portfolio | 4,818 |

| | 10,257 |

| | 3,402 |

| | 2,303 |

| | — |

| | — |

| | 20,780 |

|

Non same-store - acquired and in development(1) | — |

| | — |

| | 123 |

| | 130 |

| | — |

| | — |

| | 253 |

|

Total | 4,818 |

| | 10,257 |

| | 3,525 |

| | 2,433 |

| | — |

| | — |

| | 21,033 |

|

| | | | | | | | | | | | | |

Net Operating Income (NOI) | | | | | | | | | | | | | |

Same-store portfolio | 7,589 |

| | 20,930 |

| | 7,877 |

| | 7,507 |

| | — |

| | — |

| | 43,903 |

|

Non same-store - acquired and in development(1) | — |

| | — |

| | (69 | ) | | 497 |

| | — |

| | — |

| | 428 |

|

Total | $ | 7,589 |

| | $ | 20,930 |

| | $ | 7,808 |

| | $ | 8,004 |

| | $ | — |

| | — |

| | $ | 44,331 |

|

| | | | | | | | | | | | | |

Same-store portfolio NOI GAAP basis (from above) | $ | 7,589 |

| | $ | 20,930 |

| | $ | 7,877 |

| | $ | 7,507 |

| | $ | — |

| | — |

| | $ | 43,903 |

|

Straight-line revenue, net for same-store properties | (12 | ) | | (680 | ) | | (145 | ) | | (89 | ) | | — |

| | — |

| | (926 | ) |

FAS 141 Min Rent | (191 | ) | | (293 | ) | | (98 | ) | | (80 | ) | | — |

| | — |

| | (662 | ) |

Amortization of lease intangibles for same-store properties | — |

| | 49 |

| | 9 |

| | 15 |

| | — |

| | — |

| | 73 |

|

Same-store portfolio NOI, cash basis | $ | 7,386 |

| | $ | 20,006 |

| | $ | 7,643 |

| | $ | 7,353 |

| | $ | — |

| | — |

| | $ | 42,388 |

|

| | | | | | | | | | | | | |

Reconciliation of NOI to net income | | | | | | | | | | | | | |

Total NOI | $ | 7,589 |

| | $ | 20,930 |

| | $ | 7,808 |

| | $ | 8,004 |

| | $ | — |

| | — |

| | $ | 44,331 |

|

Other income | — |

| | — |

| | — |

| | — |

| | — |

| | 318 |

| | 318 |

|

Acquisition costs | — |

| | — |

| | — |

| | — |

| | — |

| | (709 | ) | | (709 | ) |

Interest expense | (1,725 | ) | | (2,270 | ) | | (1,347 | ) | | (322 | ) | | — |

| | (11,903 | ) | | (17,567 | ) |

Depreciation and amortization | (3,312 | ) | | (10,945 | ) | | (3,939 | ) | | (1,971 | ) | | — |

| | (325 | ) | | (20,492 | ) |

General and administrative | — |

| | — |

| | — |

| | — |

| | — |

| | (3,951 | ) | | (3,951 | ) |

Loss on extinguishment of debt | — |

| | — |

| | — |

| | — |

| | — |

| | (8,896 | ) | | (8,896 | ) |

Gain from non-disposal activities | — |

| | — |

| | — |

| | — |

| | — |

| | 3 |

| | 3 |

|

Discontinued operations(2) | — |

| | 607 |

| | — |

| | — |

| | 3,314 |

| | — |

| | 3,921 |

|

Gain on sale of real estate | — |

| | — |

| | — |

| | — |

| | — |

| | 13,657 |

| | 13,657 |

|

Net income | 2,552 |

| | 8,322 |

| | 2,522 |

| | 5,711 |

| | 3,314 |

| | (11,806 | ) | | 10,615 |

|

Net income attributable to noncontrolling interests | — |

| | — |

| | — |

| | — |

| | — |

| | (24 | ) | | (24 | ) |

Net income attributable to the controlling interests | $ | 2,552 |

| | $ | 8,322 |

| | $ | 2,522 |

| | $ | 5,711 |

| | $ | 3,314 |

| | $ | (11,830 | ) | | $ | 10,591 |

|

| | | | | | | | | | | | | |

(1) Non same-store properties were:

Acquisitions:

Office - Quantico Corporate Center

Retail - Gateway Overlook

Medical Office - Lansdowne Medical Office Building.

(2) Discontinued operations included the following held for sale and sold properties:

Office - Dulles Station, Phase I and The Ridges

Industrial/Office - Ammendale I & II, Amvax and the Industrial Portfolio (see Supplemental Definitions for list of properties).

|

| | |

Same-Store Net Operating Income (NOI) Detail (In thousands) |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Twelve Months Ended December 31, 2011 |

| | Multifamily | | Office | | Medical Office | | Retail | | Industrial/Flex | | Corporate and Other | | Total |

Real estate rental revenue | | | | | | | | | | | | | | |

Same-store portfolio | | $ | 50,979 |

| | $ | 117,161 |

| | $ | 44,627 |

| | $ | 40,872 |

| | $ | — |

| | — |

| | $ | 253,639 |

|

Non same-store - acquired and in development 1 | | — |

| | 25,709 |

| | 630 |

| | 9,549 |

| | — |

| | — |

| | 35,888 |

|

Total | | 50,979 |

| | 142,870 |

| | 45,257 |

| | 50,421 |

| | — |

| | — |

| | 289,527 |

|

| | | | | | | | | | | | | | |

Real estate expenses | | | | | | | | | | | | | | |

Same-store portfolio | | 19,717 |

| | 39,974 |

| | 13,644 |

| | 12,023 |

| | — |

| | — |

| | 85,358 |

|

Non same-store - acquired and in development 1 | | — |

| | 8,986 |

| | 598 |

| | 2,250 |

| | — |

| | — |

| | 11,834 |

|

Total | | 19,717 |

| | 48,960 |

| | 14,242 |

| | 14,273 |

| | — |

| | — |

| | 97,192 |

|

| | | | | | | | | | | | | | |

Net Operating Income (NOI) | | | | | | | | | | | | | | |

Same-store portfolio | | 31,262 |

| | 77,187 |

| | 30,983 |

| | 28,849 |

| | — |

| | — |

| | 168,281 |

|

Non same-store - acquired and in development 1 | | — |

| | 16,723 |

| | 32 |

| | 7,299 |

| | — |

| | — |

| | 24,054 |

|

Total | | $ | 31,262 |

| | $ | 93,910 |

| | $ | 31,015 |

| | $ | 36,148 |

| | $ | — |

| | — |

| | $ | 192,335 |

|

| | | | | | | | | | | | | | |

Same-store portfolio NOI GAAP basis (from above) | | $ | 31,262 |

| | $ | 77,187 |

| | $ | 30,983 |

| | $ | 28,849 |

| | $ | — |

| | — |

| | $ | 168,281 |

|

Straight-line revenue, net for same-store properties | | (32 | ) | | (1,111 | ) | | (617 | ) | | 84 |

| | — |

| | — |

| | (1,676 | ) |

FAS 141 Min Rent | | (766 | ) | | (1,164 | ) | | (383 | ) | | (342 | ) | | — |

| | — |

| | (2,655 | ) |

Amortization of lease intangibles for same-store properties | | — |

| | 486 |

| | 39 |

| | 125 |

| | — |

| | — |

| | 650 |

|

Same-store portfolio NOI, cash basis | | $ | 30,464 |

| | $ | 75,398 |

| | $ | 30,022 |

| | $ | 28,716 |

| | $ | — |

| | — |

| | $ | 164,600 |

|

| | | | | | | | | | | | | | |

Reconciliation of NOI to Net Income | | | | | | | | | | | | | | |

Total NOI | | $ | 31,262 |

| | $ | 93,910 |

| | $ | 31,015 |

| | $ | 36,148 |

| | $ | — |

| | — |

| | $ | 192,335 |

|

Other income | | — |

| | — |

| | — |

| | — |

| | — |

| | 1,144 |

| | 1,144 |

|

Acquisition costs | | — |

| | — |

| | — |

| | — |

| | — |

| | (3,607 | ) | | (3,607 | ) |

Interest expense | | (6,824 | ) | | (9,957 | ) | | (5,071 | ) | | (1,653 | ) | | — |

| | (42,968 | ) | | (66,473 | ) |

Depreciation and amortization | | (12,620 | ) | | (51,644 | ) | | (15,483 | ) | | (12,158 | ) | | — |

| | (1,392 | ) | | (93,297 | ) |

General and administrative | | — |

| | — |

| | — |

| | — |

| | — |

| | (15,728 | ) | | (15,728 | ) |

Real estate impairment | | — |

| | — |

| | — |

| | — |

| | — |

| | (14,526 | ) | | (14,526 | ) |

Gain (loss) on extinguishment of debt | | — |

| | — |

| | — |

| | — |

| | — |

| | (976 | ) | | (976 | ) |

Gain on non disposal | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

|

Discontinued operations 2 | | — |

| | 107 |

| | — |

| | — |

| | 10,046 |

| | — |

| | 10,153 |

|

Gain on sale of real estate | | — |

| | — |

| | — |

| | — |

| | — |

| | 97,491 |

| | 97,491 |

|

Income tax expense on sale of real estate | | — |

| | — |

| | — |

| | — |

| | — |

| | (1,138 | ) | | (1,138 | ) |

Net Income | | 11,818 |

| | 32,416 |

| | 10,461 |

| | 22,337 |

| | 10,046 |

| | 18,300 |

| | 105,378 |

|

Net income attributable to noncontrolling interests | | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | (494 | ) | | $ | (494 | ) |

Net income attributable to the controlling interests | | 11,818 |

| | 32,416 |

| | 10,461 |

| | 22,337 |

| | 10,046 |

| | 17,806 |

| | 104,884 |

|

(1) Non same-store properties were:

Acquisitions:

Office - Quantico Corporate Center, 1140 Connecticut Avenue, 1227 25th Street, Braddock Metro Center and John Marshall II.

Retail - Gateway Overlook, Olney Village Center.

Medical Office - Lansdowne Medical Office Building.

(2) Discontinued operations included the following held for sale and sold properties:

Office - Parklawn Plaza, Saratoga , Lexington, The Ridges, Dulles Station, Phase I.

Industrial/Office - Charleston Business Center, Ammendale I&II, Amvax and the Industrial Portfolio (see Supplemental Definitions for list of properties).

|

| | | | |

Same-Store Net Operating Income (NOI) Detail (In thousands) | | |

|

| | | | | | | | | | | | | | | | | | | | | |

| | Twelve Months Ended December 31, 2010 |

| | Multifamily | | Office | | Medical Office | | Retail | | Industrial/Flex | | Corporate and Other | | Total |

Real estate rental revenue | | | | | | | | | | | | | | |

Same-store portfolio | | 48,599 |

| | 118,913 |

| | 44,949 |

| | 40,376 |

| | — |

| | — |

| | 252,837 |

|

Non same-store - acquired and in development 1 | | — |

| | 4,947 |

| | 79 |

| | 627 |

| | — |

| | — |

| | 5,653 |

|

Total | | 48,599 |

| | 123,860 |

| | 45,028 |

| | 41,003 |

| | — |

| | — |

| | 258,490 |

|

| | | | | | | | | | | | | | |

Real estate expenses | | | | | | | | | | | | | | |

Same-store portfolio | | 19,243 |

| | 41,095 |

| | 14,205 |

| | 10,180 |

| | — |

| | — |

| | 84,723 |

|

Non same-store - acquired and in development 1 | | — |

| | 1,297 |

| | 510 |

| | 130 |

| | — |

| | — |

| | 1,937 |

|

Total | | 19,243 |

| | 42,392 |

| | 14,715 |

| | 10,310 |

| | — |

| | — |

| | 86,660 |

|

| | | | | | | | | | | | | | |

Net Operating Income (NOI) | | | | | | | | | | | | | | |

Same-store portfolio | | 29,356 |

| | 77,818 |

| | 30,744 |

| | 30,196 |

| | — |

| | — |

| | 168,114 |

|

Non same-store - acquired and in development 1 | | — |

| | 3,650 |

| | (431 | ) | | 497 |

| | — |

| | — |

| | 3,716 |

|

Total | | 29,356 |

| | 81,468 |

| | 30,313 |

| | 30,693 |

| | — |

| | — |

| | 171,830 |

|

| | | | | | | | | | | | | | |

Same-store portfolio NOI GAAP basis (from above) | | 29,356 |

| | 77,818 |

| | 30,744 |

| | 30,196 |

| | — |

| | — |

| | 168,114 |

|

Straight-line revenue, net for same-store properties | | (40 | ) | | (2,208 | ) | | (447 | ) | | (109 | ) | | — |

| | — |

| | (2,804 | ) |

FAS 141 Min Rent | | (766 | ) | | (1,607 | ) | | (401 | ) | | (323 | ) | | — |

| | — |

| | (3,097 | ) |

Amortization of lease intangibles for same-store properties | | — |

| | 154 |

| | 28 |

| | 44 |

| | — |

| | — |

| | 226 |

|

Same-store portfolio NOI, cash basis | | 28,550 |

| | 74,157 |

| | 29,924 |

| | 29,808 |

| | — |

| | — |

| | 162,439 |

|

| | | | | | | | | | | | | | |

Reconciliation of NOI to Net Income | | | | | | | | | | | | | | |

Total NOI | | 29,356 |

| | 81,468 |

| | 30,313 |

| | 30,693 |

| | — |

| | — |

| | 171,830 |

|

Other income | | — |

| | — |

| | — |

| | — |

| | — |

| | 1,193 |

| | 1,193 |

|

Acquisition costs | | — |

| | — |

| | — |

| | — |

| | — |

| | (1,161 | ) | | (1,161 | ) |

Interest expense | | (6,853 | ) | | (9,039 | ) | | (5,391 | ) | | (1,287 | ) | | — |

| | (44,659 | ) | | (67,229 | ) |

Depreciation and amortization | | (13,635 | ) | | (42,301 | ) | | (15,514 | ) | | (7,314 | ) | | — |

| | (1,302 | ) | | (80,066 | ) |

General and administrative | | — |

| | — |

| | — |

| | — |

| | — |

| | (14,406 | ) | | (14,406 | ) |

Gain (loss) on extinguishment of debt | | — |

| | — |

| | — |

| | — |

| | — |

| | (9,176 | ) | | (9,176 | ) |

Gain on non disposal | | — |

| | — |

| | — |

| | — |

| | — |

| | 7 |

| | 7 |

|

Discontinued operations 2 | | — |

| | 1,968 |

| | — |

| | — |

| | 13,000 |

| | — |

| | 14,968 |

|

Gain on sale of real estate | | — |

| | — |

| | — |

| | — |

| | — |

| | 21,599 |

| | 21,599 |

|

Income tax expense on sale of real estate | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

|

Net Income | | 8,868 |

| | 32,096 |

| | 9,408 |

| | 22,092 |

| | 13,000 |

| | (47,905 | ) | | 37,559 |

|

Net income attributable to noncontrolling interests | | — |

| | — |

| | — |

| | — |

| | — |

| | (133 | ) | | (133 | ) |

Net income attributable to the controlling interests | | 8,868 |

| | 32,096 |

| | 9,408 |

| | 22,092 |

| | 13,000 |

| | (48,038 | ) | | 37,426 |

|

| | | | | | | | | | | | | | |

1) Non same-store properties were:

Acquisitions:

Office - Quantico Corporate Center

Retail - Gateway Overlook

Medical Office - Lansdowne Medical Office Building.

(2) Discontinued operations included the following held for sale and sold properties:

Office - Parklawn Plaza, Saratoga , Lexington, The Ridges, Dulles Station, Phase I.

Industrial/Office - Charleston Business Center, Ammendale I&II, Amvax and the Industrial Portfolio (see Supplemental Definitions for list of properties).

|

| | | | |

Net Operating Income (NOI) by Region | | |

|

| | | | | | | | | | | | | | |

| | | | | | | | | | |

WRIT Portfolio | | WRIT Portfolio |

Maryland/Virginia/DC | | Inside & Outside the Beltway |

| | | | | | | | | | |

| | | | | | | | | | |

| | Percentage of

Q4 2011 GAAP NOI | | Percentage of

YTD 2011 GAAP NOI | | | | Percentage of

Q4 2011 GAAP NOI | | Percentage of

YTD 2011 GAAP NOI |

| | | | | | | | | | |

DC | | | | | | Inside the Beltway | | |

Multifamily | | 3.8 | % | | 4.0 | % | | Multifamily | | 15.0 | % | | 15.4 | % |

Office | | 17.6 | % | | 19.2 | % | | Office | | 27.0 | % | | 26.5 | % |

Medical Office | | 1.7 | % | | 1.9 | % | | Medical Office | | 3.0 | % | | 3.2 | % |

Retail | | 0.7 | % | | 0.7 | % | | Retail | | 6.3 | % | | 6.6 | % |

| | 23.8 | % | | 25.8 | % | | | | 51.3 | % | | 51.7 | % |

| | | | | | | | | | |

Maryland | | | | | | Outside the Beltway | | |

Multifamily | | 2.6 | % | | 2.5 | % | | Multifamily | | 0.8 | % | | 0.9 | % |

Office | | 11.5 | % | | 12.4 | % | | Office | | 23.1 | % | | 22.2 | % |

Medical Office | | 4.4 | % | | 4.6 | % | | Medical Office | | 12.3 | % | | 13.0 | % |

Retail | | 12.9 | % | | 12.3 | % | | Retail | | 12.5 | % | | 12.2 | % |

| | 31.4 | % | | 31.8 | % | | | | 48.7 | % | | 48.3 | % |

| | | | | | | | | | |

Virginia | | | | | | Total Portfolio | | 100.0 | % | | 100.0 | % |

Multifamily | | 9.5 | % | | 9.8 | % | | | | | | |

Office | | 21.0 | % | | 17.2 | % | | | | | | |

Medical Office | | 9.2 | % | | 9.6 | % | | | | | | |

Retail | | 5.1 | % | | 5.8 | % | | | | | | |

| | 44.8 | % | | 42.4 | % | | | | | | |

| | | | | | | | | | |

Total Portfolio | | 100.0 | % | | 100.0 | % | | | | | | |

|

| | | | |

Same-Store and Overall Physical Occupancy Levels by Sector

| |

|

| | | | | | | | | | | | | | | |

| | Physical Occupancy - Same-Store Properties (1) |

Sector | | 12/31/2011 | | 9/30/2011 | | 6/30/2011 | | 3/31/2011 | | 12/31/2010 |

| | | | | | | | | | |

Multifamily | | 94.9 | % | | 94.0 | % | | 95.6 | % | | 95.3 | % | | 95.7 | % |

Office Buildings | | 88.8 | % | | 88.1 | % | | 88.4 | % | | 89.3 | % | | 89.4 | % |

Medical Office Buildings | | 90.6 | % | | 91.3 | % | | 91.7 | % | | 93.5 | % | | 93.8 | % |

Retail Centers | | 93.0 | % | | 91.8 | % | | 92.3 | % | | 92.2 | % | | 92.5 | % |

Industrial / Flex | | — | % | | — | % | | — | % | | — | % | | — | % |

| | | | | | | | | | |

Overall Portfolio | | 91.3 | % | | 90.7 | % | | 91.3 | % | | 91.8 | % | | 92.1 | % |

| | | | | | | | | | |

| | Physical Occupancy - All Properties |

Sector | | 12/31/2011 | | 9/30/2011 | | 6/30/2011 | | 3/31/2011 | | 12/31/2010 |

| | | | | | | | | | |

Multifamily | | 94.9 | % | | 94.0 | % | | 95.6 | % | | 95.3 | % | | 95.7 | % |

Office Buildings | | 89.0 | % | | 88.6 | % | | 88.1 | % | | 89.1 | % | | 89.4 | % |

Medical Office Buildings | | 86.5 | % | | 87.2 | % | | 87.3 | % | | 88.3 | % | | 88.5 | % |

Retail Centers | | 93.3 | % | | 92.3 | % | | 92.0 | % | | 92.0 | % | | 92.1 | % |

Industrial / Flex | | — | % | | 75.4 | % | | 78.4 | % | | 80.2 | % | | 78.6 | % |

| | | | | | | | | | |

Overall Portfolio | | 90.8 | % | | 89.0 | % | | 87.7 | % | | 88.5 | % | | 88.3 | % |

(1) Non same-store properties were:

Acquisitions:

Office - 1140 Connecticut Avenue, 1227 25th Street, Braddock Metro Center and John Marshall II.

Retail - Gateway Overlook, Olney Village Center.

Medical Office - Lansdowne Medical Office Building.

Held for sale and sold properties:

Office - The Ridges.

Industrial/Office - Ammendale I & II, Amvax and the Industrial Portfolio (see Supplemental Definitions for list of properties).

|

| | | | |

Same-Store Portfolio and Overall Economic Occupancy Levels by Sector | |

|

| | | | | | | | | | | | | | | |

| | Economic Occupancy - Same-Store Properties(1) |

Sector | | 12/31/2011 | | 9/30/2011 | | 6/30/2011 | | 3/31/2011 | | 12/31/2010 |

| | | | | | | | | | |

Multifamily | | 94.2 | % | | 94.1 | % | | 94.9 | % | | 94.8 | % | | 95.5 | % |

Office Buildings | | 89.8 | % | | 89.2 | % | | 90.2 | % | | 90.3 | % | | 89.7 | % |

Medical Office Buildings | | 92.4 | % | | 92.8 | % | | 94.0 | % | | 94.2 | % | | 94.5 | % |

Retail Centers | | 92.3 | % | | 92.0 | % | | 92.3 | % | | 92.3 | % | | 91.4 | % |

Industrial / Flex | | — | % | | — | % | | — | % | | — | % | | — | % |

| | | | | | | | | | |

Overall Portfolio | | 91.5 | % | | 91.2 | % | | 92.1 | % | | 92.1 | % | | 91.9 | % |

| | | | | | | | | | |

| | Economic Occupancy - All Properties |

Sector | | 12/31/2011 | | 9/30/2011 | | 6/30/2011 | | 3/31/2011 | | 12/31/2010 |

| | | | | | | | | | |

Multifamily | | 94.2 | % | | 94.1 | % | | 94.9 | % | | 94.8 | % | | 95.5 | % |

Office Buildings | | 89.4 | % | | 88.5 | % | | 89.7 | % | | 90.7 | % | | 90.0 | % |

Medical Office Buildings | | 89.5 | % | | 89.9 | % | | 90.5 | % | | 90.5 | % | | 90.3 | % |

Retail Centers | | 93.0 | % | | 92.3 | % | | 92.3 | % | | 92.0 | % | | 91.4 | % |

Industrial / Flex | | 79.3 | % | | 80.8 | % | | 81.9 | % | | 81.4 | % | | 81.9 | % |

| | | | | | | | | | |

Overall Portfolio | | 90.8 | % | | 89.5 | % | | 90.2 | % | | 90.5 | % | | 90.2 | % |

(1) Non same-store properties were:

Acquisitions:

Office - 140 Connecticut Avenue, 1227 25th Street, Braddock Metro Center and John Marshall II.

Retail - Gateway Overlook, Olney Village Center.

Medical Office - Lansdowne Medical Office Building.

Held for sale and sold properties:

Office - The Ridges.

Industrial/Office - Ammendale I & II, Amvax and the Industrial Portfolio (see Supplemental Definitions for list of properties).

|

| | | | |

Commercial Leasing Summary | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 4th Quarter 2011 | | 3rd Quarter 2011 | | 2nd Quarter 2011 | | 1st Quarter 2011 | | 4th Quarter 2010 |

Gross Leasing Square Footage | | | | | | | | | | | | | | | | | | | | |

Office Buildings | | 175,032 | | 152,900 | | 160,318 | | 138,083 | | 125,367 |

Medical Office Buildings | | 65,162 | | 29,070 | | 61,374 | | 43,355 | | 7,136 |

Retail Centers | | 23,375 | | 59,910 | | 38,482 | | 78,669 | | 97,055 |

Total | | 263,569 | | 241,880 | | 260,174 | | 260,107 | | 229,558 |

Weighted Average Term (yrs) | | | | | | | | | | | | | | | | | | | | |

Office Buildings | | 4.8 | | 4.3 | | 7.5 | | 3.6 | | 5.4 |

Medical Office Buildings | | 4.4 | | 4.9 | | 5.5 | | 6.0 | | 3.9 |

Retail Centers | | 5.9 | | 5.9 | | 8.2 | | 4.5 | | 8.4 |

Total | | 4.8 | | 4.7 | | 7.1 | | 4.3 | | 6.6 |

| | | | | | | | | | | | | | | | | | | | |

Rental Rate Increases: | | GAAP | | CASH | | GAAP | | CASH | | GAAP | | CASH | | GAAP | | CASH | | GAAP | | CASH |

Rate on expiring leases | | | | | | | | | | | | | | | | | | | | |

Office Buildings | | $ | 30.22 |

| | $ | 31.94 |

| | $ | 36.04 |

| | $ | 37.87 |

| | $ | 25.59 |

| | $ | 26.66 |

| | $ | 31.41 |

| | $ | 32.26 |

| | $ | 28.72 |

| | $ | 30.30 |

|

Medical Office Buildings | | 34.70 |

| | 37.70 |

| | 34.63 |

| | 36.79 |

| | 30.74 |

| | 32.36 |

| | 32.91 |

| | 34.90 |

| | 35.53 |

| | 37.37 |

|

Retail Centers | | 22.12 |

| | 23.02 |

| | 14.14 |

| | 17.39 |

| | 23.67 |

| | 24.20 |

| | 15.64 |

| | 15.91 |

| | 15.50 |

| | 16.13 |

|

Total | | $ | 30.61 |

| | $ | 32.57 |

| | $ | 30.19 |

| | $ | 32.41 |

| | $ | 26.53 |

| | $ | 27.65 |

| | $ | 26.89 |

| | $ | 27.76 |

| | $ | 23.34 |

| | $ | 24.53 |

|

| | | | | | | | | | | | | | | | | | | | |

Rate on new leases | | | | | | | | | | | | | | | | | | | | |

Office Buildings | | $ | 31.38 |

| | $ | 29.66 |

| | $ | 39.53 |

| | $ | 37.76 |

| | $ | 29.06 |

| | $ | 26.64 |

| | $ | 30.97 |

| | $ | 29.91 |

| | $ | 31.39 |

| | $ | 29.41 |

|

Medical Office Buildings | | 38.91 |

| | 37.13 |

| | 37.76 |

| | 35.79 |

| | 36.13 |

| | 33.64 |

| | 37.24 |

| | 34.76 |

| | 37.41 |

| | 36.05 |

|

Retail Centers | | 28.89 |

| | 26.86 |

| | 18.56 |

| | 21.96 |

| | 25.88 |

| | 24.34 |

| | 16.48 |

| | 16.30 |

| | 21.79 |

| | 20.41 |

|

Total | | $ | 33.02 |

| | $ | 31.26 |

| | $ | 33.71 |

| | $ | 33.24 |

| | $ | 30.25 |

| | $ | 27.96 |

| | $ | 27.63 |

| | $ | 26.60 |

| | $ | 27.52 |

| | $ | 25.81 |

|

| | | | | | | | | | | | | | | | | | | | |

Percentage Increase | | | | | | | | | | | | | | | | | | | | |

Office Buildings | | 3.82 | % | | (7.15 | )% | | 9.69 | % | | (0.30 | )% | | 13.58 | % | | (0.10 | )% | | (1.40 | )% | | (7.30 | )% | | 9.31 | % | | (2.93 | )% |

Medical Office Buildings | | 12.14 | % | | (1.51 | )% | | 9.04 | % | | (2.70 | )% | | 17.51 | % | | 3.96 | % | | 13.14 | % | | (0.41 | )% | | 5.28 | % | | (3.53 | )% |

Retail Centers | | 30.63 | % | | 16.71 | % | | 31.29 | % | | 26.25 | % | | 9.34 | % | | 0.60 | % | | 5.39 | % | | 2.42 | % | | 40.57 | % | | 26.50 | % |

Total | | 7.87 | % | | (4.04 | )% | | 11.66 | % | | 2.56 | % | | 14.06 | % | | 1.13 | % | | 2.76 | % | | (4.17 | )% | | 17.90 | % | | 5.22 | % |

|

| | | | |

Commercial Leasing Summary Tenant Improvements and Leasing Costs | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 4th Quarter 2011 | | 3rd Quarter 2011 | | 2nd Quarter 2011 | | 1st Quarter 2011 | | 4th Quarter 2010 |

| | | | | | | | | | | | | | | | | | | | |

| | Total Dollars | | Dollars per Square Foot | | Total Dollars | | Dollars per Square Foot | | Total Dollars | | Dollars per Square Foot | | Total Dollars | | Dollars per Square Foot | | Total Dollars | | Dollars per Square Foot |

Tenant Improvements | | | | | | | | | | | | | | | | | | | | |

Office Buildings | | $ | 3,691,099 |

| | $ | 21.09 |

| | $ | 2,067,782 |

| | $ | 13.52 |

| | $ | 3,019,025 |

| | $ | 18.83 |

| | $ | 535,261 |

| | $ | 3.88 |

| | $ | 2,461,268 |

| | $ | 19.63 |

|

Medical Office Buildings | | 788,535 |

| | 12.10 |

| | 112,145 |

| | 3.86 |

| | 893,785 |

| | 14.56 |

| | 384,334 |

| | 8.86 |

| | 86,937 |

| | 12.18 |

|

Retail Centers | | 25,740 |

| | 1.10 |

| | 1,424,151 |

| | 23.77 |

| | 265,135 |

| | 6.89 |

| | — |

| | — |

| | 288,110 |

| | 2.97 |

|

Subtotal | | $ | 4,505,374 |

| | $ | 17.09 |

| | $ | 3,604,078 |

| | $ | 14.90 |

| | $ | 4,177,945 |

| | $ | 16.06 |

| | $ | 919,595 |

| | $ | 3.54 |

| | $ | 2,836,315 |

| | $ | 12.36 |

|

| | | | | | | | | | | | | | | | | | | | |

Leasing Costs | | | | | | | | | | | | | | | | | | | | |

Office Buildings | | $ | 2,133,927 |

| | $ | 12.19 |

| | $ | 1,596,565 |

| | $ | 10.44 |

| | $ | 2,189,912 |

| | $ | 13.66 |

| | $ | 582,007 |

| | $ | 4.21 |

| | $ | 1,478,762 |

| | $ | 11.80 |

|

Medical Office Buildings | | 400,976 |

| | 6.15 |

| | 206,298 |

| | 7.10 |

| | 716,648 |

| | 11.68 |

| | 530,073 |

| | 12.23 |

| | 21,352 |

| | 2.99 |

|

Retail Centers | | 178,127 |

| | 7.62 |

| | 504,673 |

| | 8.42 |

| | 269,557 |

| | 7.00 |

| | 77,260 |

| | 0.98 |

| | 416,203 |

| | 4.29 |

|

Subtotal | | $ | 2,713,030 |

| | $ | 10.29 |

| | $ | 2,307,536 |

| | $ | 9.54 |

| | $ | 3,176,117 |

| | $ | 12.21 |

| | $ | 1,189,340 |

| | $ | 4.57 |

| | $ | 1,916,317 |

| | $ | 8.35 |

|

| | | | | | | | | | | | | | | | | | | | |

Tenant Improvements and Leasing Costs | | | | | | | | | | | | | | | | | | |

Office Buildings | | $ | 5,825,026 |

| | $ | 33.28 |

| | $ | 3,664,347 |

| | $ | 23.96 |

| | $ | 5,208,937 |

| | $ | 32.49 |

| | $ | 1,117,268 |

| | $ | 8.09 |

| | $ | 3,940,030 |

| | $ | 31.43 |

|

Medical Office Buildings | | 1,189,511 |

| | 18.25 |

| | 318,443 |

| | 10.96 |

| | 1,610,433 |

| | 26.24 |

| | 914,407 |

| | 21.09 |

| | 108,289 |

| | 15.17 |

|

Retail Centers | | 203,867 |

| | 8.72 |

| | 1,928,824 |

| | 32.19 |

| | 534,692 |

| | 13.89 |

| | 77,260 |

| | 0.98 |

| | 704,313 |

| | 7.26 |

|

Total | | $ | 7,218,404 |

| | $ | 27.38 |

| | $ | 5,911,614 |

| | $ | 24.44 |

| | $ | 7,354,062 |

| | $ | 28.27 |

| | $ | 2,108,935 |

| | $ | 8.11 |

| | $ | 4,752,632 |

| | $ | 20.71 |

|

|

| | | | |

10 Largest Tenants - Based on Annualized Rent December 31, 2011 | | |

|

| | | | | | | | | | | | | | |

Tenant | Number of Buildings | | Weighted Average Remaining Lease Term in Months | | Percentage of Aggregate Portfolio Annualized Rent | | Aggregate Rentable Square Feet | | Percentage of Aggregate Occupied Square Feet |

| | | | | | | | | |

World Bank | 1 |

| | 42 |

| | 5.09 | % | | 210,354 |

| | 2.90 | % |

General Services Administration | 6 |

| | 34 |

| | 2.99 | % | | 170,834 |

| | 2.36 | % |

Advisory Board Company | 1 |

| | 89 |

| | 2.89 | % | | 180,925 |

| | 2.49 | % |

L-3 Services, Inc. | 1 |

| | 66 |

| | 2.34 | % | | 147,468 |

| | 2.03 | % |

Booz Allen Hamilton, Inc. | 1 |

| | 49 |

| | 2.29 | % | | 222,989 |

| | 3.07 | % |

Patton Boggs LLP | 1 |