|

| | | | | | |

| |

| Washington Real Estate Investment Trust | |

| First Quarter 2017 | |

| | |

| Supplemental Operating and Financial Data | |

| Contact: | | 1775 Eye Street, NW | |

| Tejal R. Engman | | Suite 1000 | |

| Director of Investor Relations | | Washington, DC 20006 | |

| E-mail: tengman@washreit.com | | (202) 774-3200 | |

| | | (301) 984-9610 fax | |

| | | | | | |

|

|

Company Background and Highlights |

First Quarter 2017 |

Washington Real Estate Investment Trust ("Washington REIT") is a self-administered equity real estate investment trust investing in income-producing properties in the greater Washington, DC region. Washington REIT has a diversified portfolio with investments in office, retail, and multifamily properties and land for development.

First Quarter 2017 Highlights

Net income attributable to controlling interests was $6.6 million, or $0.09 per diluted share, compared to $2.4 million, or $0.03 per diluted share, in the first quarter 2016. NAREIT Funds from Operations (FFO) of $32.7 million, or $0.43 per diluted share, compared to $28.4 million, or $0.41 per diluted share in the first quarter of 2016. Additional highlights are as below:

| |

• | Reported Core FFO of $0.44 per diluted share |

| |

• | Grew same-store Net Operating Income (NOI) by 10.4% year-over-year |

| |

• | Grew same-store NOI by 15.6% for the office, 7.9% for the retail and 4.0% for the multifamily portfolios year-over-year |

| |

• | Increased same-store ending occupancy by 320 basis points year-over-year to 93.7% |

| |

• | Announced the acquisition of Watergate 600, a 309,000 square foot office building in Washington, DC for $135.0 million in a transaction completed subsequent to quarter-end |

| |

• | Raised the bottom and top ends of the 2017 Core FFO guidance range by two cents to $1.76 to $1.84 from $1.74 to $1.82 per diluted share |

Of the 195,000 square feet of commercial leases signed, there were 44,000 square feet of new leases and 151,000 square feet of renewal leases. New leases had an average rental rate increase of 25.6% over expiring lease rates and a weighted average lease term of 8.1 years. Commercial tenant improvement costs were $53.84 per square foot and leasing commissions were $17.72 per square foot for new leases. Renewal leases had an average rental rate increase of 22.7% from expiring lease rates and a weighted average lease term of 9.9 years. Commercial tenant improvement costs were $64.76 per square foot and leasing commissions were $20.58 per square foot for renewal leases.

On April 4, 2017, Washington REIT completed the acquisition of Watergate 600, a 309,000 square foot iconic office building on the Potomac riverfront in Washington, DC for $135.0 million in a transaction that is structured to include the issuance of units for a portion of the purchase price.

In January 2017, Washington REIT refinanced pre-payable and maturing secured debt by drawing the remaining $50.0 million on the seven-year $150.0 million unsecured term loan, which is scheduled to mature in July, 2023. Washington REIT entered into a forward swap from floating interest rates to a 2.86% all-in fixed interest rate for $150.0 million commencing on March 31, 2017.

Year-to-date, the Company issued 2,070,000 shares at an average price of $31.44 per share through the Company’s At-the-Market (ATM) program, raising gross proceeds of $65.1 million to maintain balance sheet strength.

As of March 31, 2017, Washington REIT owned a diversified portfolio of 49 properties, totaling approximately 6 million square feet of commercial space and 4,480 multifamily units, and land held for development. These 49 properties consist of 19 office properties, 16 retail centers and 14 multifamily properties. Washington REIT shares are publicly traded on the New York Stock Exchange (NYSE:WRE).

|

|

Company Background and Highlights |

First Quarter 2017 |

Net Operating Income Contribution by Sector - First Quarter 2017

Certain statements in our earnings release and on our conference call are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements in this earnings release preceded by, followed by or that include the words “believe,” “expect,” “intend,” “anticipate,” “potential,” “project,” “will” and other similar expressions. Such statements involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially. Such risks, uncertainties and other factors include, but are not limited to, the potential for federal government budget reductions, changes in general and local economic and real estate market conditions, the timing and pricing of lease transactions, the availability and cost of capital, fluctuations in interest rates, tenants' financial conditions, levels of competition, the effect of government regulation, the impact of newly adopted accounting principles, and other risks and uncertainties detailed from time to time in our filings with the SEC, including our 2016 Form 10-K and subsequent Quarterly Reports on Form 10-Q. We assume no obligation to update or supplement forward-looking statements that become untrue because of subsequent events.

|

| | |

Supplemental Financial and Operating Data

Table of Contents |

March 31, 2017 |

| | |

Schedule | Page |

Key Financial Data | |

| | |

| | |

| | |

| | |

| | |

Capital Analysis | |

| Long Term Debt Analysis | |

| | |

| | |

| | |

Portfolio Analysis | |

| | |

| | |

| | |

| Same-Store Portfolio and Overall Ending Occupancy Levels by Sector | |

| | |

Growth and Strategy | |

| | |

Tenant Analysis | |

| | |

| | |

| | |

| | |

| | |

Appendix | |

| | |

| | |

|

| |

Consolidated Statements of Operations (In thousands, except per share data) (Unaudited)

| |

|

| | | | | | | | | | | | | | | | | | | |

| Three Months Ended |

OPERATING RESULTS | 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Real estate rental revenue | $ | 77,501 |

| | $ | 76,952 |

| | $ | 79,770 |

| | $ | 79,405 |

| | $ | 77,137 |

|

Real estate expenses | (27,863 | ) | | (28,940 | ) | | (29,164 | ) | | (28,175 | ) | | (28,734 | ) |

| 49,638 |

| | 48,012 |

| | 50,606 |

| | 51,230 |

| | 48,403 |

|

Real estate depreciation and amortization | (26,069 | ) | | (26,302 | ) | | (30,905 | ) | | (25,161 | ) | | (26,038 | ) |

Income from real estate | 23,569 |

| | 21,710 |

| | 19,701 |

| | 26,069 |

| | 22,365 |

|

Interest expense | (11,405 | ) | | (11,773 | ) | | (13,173 | ) | | (13,820 | ) | | (14,360 | ) |

Other income | 77 |

| | 92 |

| | 83 |

| | 83 |

| | 39 |

|

Acquisition costs | — |

| | — |

| | — |

| | (1,024 | ) | | (154 | ) |

Casualty gain | — |

| | — |

| | — |

| | 676 |

| | — |

|

Gain on sale of real estate | — |

| | — |

| | 77,592 |

| | 24,112 |

| | — |

|

General and administrative | (5,626 | ) | | (4,527 | ) | | (4,539 | ) | | (4,968 | ) | | (5,511 | ) |

Income tax (expense) benefit | — |

| | (76 | ) | | (2 | ) | | 693 |

| | — |

|

Net income | 6,615 |

| | 5,426 |

| | 79,662 |

| | 31,821 |

| | 2,379 |

|

Less: Net loss from noncontrolling interests | 19 |

| | 19 |

| | 12 |

| | 15 |

| | 5 |

|

Net income attributable to the controlling interests | $ | 6,634 |

| | $ | 5,445 |

| | $ | 79,674 |

| | $ | 31,836 |

| | $ | 2,384 |

|

Per Share Data: | | | | | | | | | |

Net income attributable to the controlling interests | $ | 0.09 |

| | $ | 0.07 |

| | $ | 1.07 |

| | $ | 0.44 |

| | $ | 0.03 |

|

Fully diluted weighted average shares outstanding | 74,966 |

| | 74,779 |

| | 74,133 |

| | 71,912 |

| | 68,488 |

|

Percentage of Revenues: | | | | | | | | | |

Real estate expenses | 36.0 | % | | 37.6 | % | | 36.6 | % | | 35.5 | % | | 37.3 | % |

General and administrative | 7.3 | % | | 5.9 | % | | 5.7 | % | | 6.3 | % | | 7.1 | % |

Ratios: | | | | | | | | | |

Adjusted EBITDA / Interest expense | 3.9 | x | | 3.7 | x | | 3.5 | x | | 3.4 | x | | 3.0 | x |

Net income attributable to the controlling interests / Real estate rental revenue | 8.6 | % | | 7.1 | % | | 99.9 | % | | 40.1 | % | | 3.1 | % |

|

| |

Consolidated Balance Sheets (In thousands) (Unaudited) | |

|

| | | | | | | | | | | | | | | | | | | |

| 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Assets | | | | | | | | | |

Land | $ | 573,315 |

| | $ | 573,315 |

| | $ | 573,315 |

| | $ | 573,315 |

| | $ | 561,256 |

|

Income producing property | 2,123,807 |

| | 2,112,088 |

| | 2,092,201 |

| | 2,072,166 |

| | 2,095,306 |

|

| 2,697,122 |

| | 2,685,403 |

| | 2,665,516 |

| | 2,645,481 |

| | 2,656,562 |

|

Accumulated depreciation and amortization | (680,231 | ) | | (657,425 | ) | | (634,945 | ) | | (613,194 | ) | | (714,689 | ) |

Net income producing property | 2,016,891 |

| | 2,027,978 |

| | 2,030,571 |

| | 2,032,287 |

| | 1,941,873 |

|

Development in progress, including land held for development | 42,914 |

| | 40,232 |

| | 37,463 |

| | 35,760 |

| | 27,313 |

|

Total real estate held for investment, net | 2,059,805 |

| | 2,068,210 |

| | 2,068,034 |

| | 2,068,047 |

| | 1,969,186 |

|

Investment in real estate held for sale, net | — |

| | — |

| | — |

| | 41,704 |

| | — |

|

Cash and cash equivalents | 15,214 |

| | 11,305 |

| | 8,588 |

| | 22,379 |

| | 23,575 |

|

Restricted cash | 1,430 |

| | 6,317 |

| | 10,091 |

| | 11,054 |

| | 9,889 |

|

Rents and other receivables, net of allowance for doubtful accounts | 69,038 |

| | 64,319 |

| | 62,989 |

| | 58,970 |

| | 63,863 |

|

Prepaid expenses and other assets | 108,622 |

| | 103,468 |

| | 100,788 |

| | 99,150 |

| | 118,790 |

|

Other assets related to properties sold or held for sale | — |

| | — |

| | — |

| | 5,147 |

| | — |

|

Total assets | $ | 2,254,109 |

| | $ | 2,253,619 |

| | $ | 2,250,490 |

| | $ | 2,306,451 |

| | $ | 2,185,303 |

|

Liabilities | | | | | | | | | |

Notes payable | $ | 893,424 |

| | $ | 843,084 |

| | $ | 744,063 |

| | $ | 743,769 |

| | $ | 743,475 |

|

Mortgage notes payable | 97,814 |

| | 148,540 |

| | 251,232 |

| | 252,044 |

| | 333,853 |

|

Lines of credit | 123,000 |

| | 120,000 |

| | 125,000 |

| | 269,000 |

| | 215,000 |

|

Accounts payable and other liabilities | 50,684 |

| | 46,967 |

| | 54,629 |

| | 52,722 |

| | 56,348 |

|

Dividend payable | — |

| | 22,414 |

| | — |

| | — |

| | — |

|

Advance rents | 11,948 |

| | 11,750 |

| | 10,473 |

| | 10,178 |

| | 11,589 |

|

Tenant security deposits | 9,002 |

| | 8,802 |

| | 8,634 |

| | 8,290 |

| | 9,604 |

|

Liabilities related to properties sold or held for sale | — |

| | — |

| | — |

| | 2,338 |

| | — |

|

Total liabilities | 1,185,872 |

| | 1,201,557 |

| | 1,194,031 |

| | 1,338,341 |

| | 1,369,869 |

|

Equity | | | | | | | | | |

Preferred shares; $0.01 par value; 10,000 shares authorized | — |

| | — |

| | — |

| | — |

| | — |

|

Shares of beneficial interest, $0.01 par value; 100,000 shares authorized | 757 |

| | 746 |

| | 745 |

| | 737 |

| | 683 |

|

Additional paid-in capital | 1,400,093 |

| | 1,368,636 |

| | 1,368,438 |

| | 1,338,101 |

| | 1,193,750 |

|

Distributions in excess of net income | (342,020 | ) | | (326,047 | ) | | (309,042 | ) | | (366,352 | ) | | (376,041 | ) |

Accumulated other comprehensive loss | 8,346 |

| | 7,611 |

| | (4,870 | ) | | (5,609 | ) | | (4,225 | ) |

Total shareholders' equity | 1,067,176 |

| | 1,050,946 |

| | 1,055,271 |

| | 966,877 |

| | 814,167 |

|

Noncontrolling interests in subsidiaries | 1,061 |

| | 1,116 |

| | 1,188 |

| | 1,233 |

| | 1,267 |

|

Total equity | 1,068,237 |

| | 1,052,062 |

| | 1,056,459 |

| | 968,110 |

| | 815,434 |

|

Total liabilities and equity | $ | 2,254,109 |

| | $ | 2,253,619 |

| | $ | 2,250,490 |

| | $ | 2,306,451 |

| | $ | 2,185,303 |

|

|

| |

Funds from Operations (In thousands, except per share data) (Unaudited)

| |

|

| | | | | | | | | | | | | | | | | | | |

| Three Months Ended |

| 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Funds from operations(1) | | | | | | | | | |

Net income | $ | 6,615 |

| | $ | 5,426 |

| | $ | 79,662 |

| | $ | 31,821 |

| | $ | 2,379 |

|

Real estate depreciation and amortization | 26,069 |

| | 26,302 |

| | 30,905 |

| | 25,161 |

| | 26,038 |

|

Gain on sale of depreciable real estate | — |

| | — |

| | (77,592 | ) | | (24,112 | ) | | — |

|

NAREIT funds from operations (FFO) | 32,684 |

| | 31,728 |

| | 32,975 |

| | 32,870 |

| | 28,417 |

|

Casualty (gain) | — |

| | — |

| | — |

| | (676 | ) | | — |

|

Severance expense | — |

| | — |

| | 242 |

| | 126 |

| | 460 |

|

Relocation expense | — |

| | — |

| | 16 |

| | — |

| | — |

|

Acquisition and structuring expenses | 215 |

| | 118 |

| | 37 |

| | 1,107 |

| | 259 |

|

Core FFO (1) | $ | 32,899 |

| | $ | 31,846 |

| | $ | 33,270 |

| | $ | 33,427 |

| | $ | 29,136 |

|

| | | | | | | | | |

Allocation to participating securities(2) | (78 | ) | | (32 | ) | | (200 | ) | | (99 | ) | | (90 | ) |

| | | | | | | | | |

NAREIT FFO per share - basic | $ | 0.44 |

| | $ | 0.42 |

| | $ | 0.44 |

| | $ | 0.46 |

| | $ | 0.41 |

|

NAREIT FFO per share - fully diluted | $ | 0.43 |

| | $ | 0.42 |

| | $ | 0.44 |

| | $ | 0.46 |

| | $ | 0.41 |

|

Core FFO per share - fully diluted | $ | 0.44 |

| | $ | 0.43 |

| | $ | 0.45 |

| | $ | 0.46 |

| | $ | 0.42 |

|

| | | | | | | | | |

Common dividend per share | $ | 0.30 |

| | $ | 0.30 |

| | $ | 0.30 |

| | $ | 0.30 |

| | $ | 0.30 |

|

| | | | | | | | | |

Average shares - basic | 74,854 |

| | 74,592 |

| | 73,994 |

| | 71,719 |

| | 68,301 |

|

Average shares - fully diluted | 74,966 |

| | 74,779 |

| | 74,133 |

| | 71,912 |

| | 68,488 |

|

(1) See "Supplemental Definitions" on page 29 of this supplemental for the definitions of FFO and Core FFO. |

(2) Adjustment to the numerators for FFO and Core FFO per share calculations when applying the two-class method for calculating EPS. |

|

| |

Funds Available for Distribution (In thousands, except per share data) (Unaudited)

| |

|

| | | | | | | | | | | | | | | | | | | |

| Three Months Ended |

| 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Funds available for distribution (FAD)(1) | | | | | | | | | |

NAREIT FFO | $ | 32,684 |

| | $ | 31,728 |

| | $ | 32,975 |

| | $ | 32,870 |

| | $ | 28,417 |

|

Tenant improvements and incentives | (5,942 | ) | | (4,822 | ) | | (4,889 | ) | | (7,639 | ) | | (1,543 | ) |

External and internal leasing commissions | (2,523 | ) | | (3,403 | ) | | (1,251 | ) | | (3,350 | ) | | (1,015 | ) |

Recurring capital improvements | (405 | ) | | (1,660 | ) | | (1,146 | ) | | (1,237 | ) | | (908 | ) |

Straight-line rent, net | (849 | ) | | (603 | ) | | (682 | ) | | (880 | ) | | (683 | ) |

Non-cash fair value interest expense | (302 | ) | | 47 |

| | 46 |

| | 44 |

| | 42 |

|

Non-real estate depreciation and amortization of debt costs | 899 |

| | 873 |

| | 846 |

| | 876 |

| | 950 |

|

Amortization of lease intangibles, net | 850 |

| | 900 |

| | 898 |

| | 853 |

| | 943 |

|

Amortization and expensing of restricted share and unit compensation | 1,130 |

| | 737 |

| | 292 |

| | 850 |

| | 1,519 |

|

Funds available for distribution (FAD) | 25,542 |

| | 23,797 |

| | 27,089 |

| | 22,387 |

| | 27,722 |

|

Non-share-based severance expense | — |

| | — |

| | 242 |

| | 126 |

| | 39 |

|

Relocation expense | — |

| | — |

| | 16 |

| | — |

| | — |

|

Acquisition and structuring expenses | 215 |

| | 118 |

| | 37 |

| | 1,107 |

| | 259 |

|

Casualty (gain) | — |

| | — |

| | — |

| | (676 | ) | | — |

|

Core FAD (1) | $ | 25,757 |

| | $ | 23,915 |

| | $ | 27,384 |

| | $ | 22,944 |

| | $ | 28,020 |

|

| | | | | | | | | |

(1) See "Supplemental Definitions" on page 29 of this supplemental for the definitions of FAD and Core FAD. |

|

| |

Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) (In thousands) (Unaudited) | |

|

| | | | | | | | | | | | | | | | | | | |

| Three Months Ended |

| 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Adjusted EBITDA (1) | | | | | | | | | |

Net income | $ | 6,615 |

| | $ | 5,426 |

| | $ | 79,662 |

| | $ | 31,821 |

| | $ | 2,379 |

|

Add: | | | | | | | | | |

Interest expense | 11,405 |

| | 11,773 |

| | 13,173 |

| | 13,820 |

| | 14,360 |

|

Real estate depreciation and amortization | 26,069 |

| | 26,302 |

| | 30,905 |

| | 25,161 |

| | 26,038 |

|

Income tax expense (benefit) | — |

| | 76 |

| | 2 |

| | (693 | ) | | — |

|

Casualty (gain) | — |

| | — |

| | — |

| | (676 | ) | | — |

|

Non-real estate depreciation | 116 |

| | 119 |

| | 101 |

| | 152 |

| | 152 |

|

Severance expense | — |

| | — |

| | 242 |

| | 126 |

| | 460 |

|

Relocation expense | — |

| | — |

| | 16 |

| | — |

| | — |

|

Acquisition and structuring expenses | 215 |

| | 118 |

| | 37 |

| | 1,107 |

| | 259 |

|

Less: | | | | | | | | | |

Net loss (gain) on sale of real estate | — |

| | — |

| | (77,592 | ) | | (24,112 | ) | | — |

|

Adjusted EBITDA | $ | 44,420 |

| | $ | 43,814 |

| | $ | 46,546 |

| | $ | 46,706 |

| | $ | 43,648 |

|

| | | | | | | | | |

(1) Adjusted EBITDA is earnings before interest expense, taxes, depreciation, amortization, gain on sale of real estate, casualty and real estate impairment, gain/loss on extinguishment of debt, severance expense, relocation expense, acquisition and structuring expense, gain from non-disposal activities and allocations to noncontrolling interests. We consider Adjusted EBITDA to be an appropriate supplemental performance measure because it permits investors to view income from operations without the effect of depreciation, and the cost of debt or non-operating gains and losses. Adjusted EBITDA is a non-GAAP measure. |

|

| |

Long Term Debt Analysis ($'s in thousands) | |

|

| | | | | | | | | | | | | | | | | | | |

| 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Balances Outstanding | | | | | | | | | |

| | | | | | | | | |

Secured | | | | | | | | | |

Mortgage note payable, net | $ | 97,814 |

| | $ | 148,540 |

| | $ | 251,232 |

| | $ | 252,044 |

| | $ | 333,853 |

|

Unsecured | | | | | | | | | |

Fixed rate bonds | 595,315 |

| | 595,067 |

| | 594,905 |

| | 594,658 |

| | 594,411 |

|

Term loans | 298,109 |

| | 248,017 |

| | 149,158 |

| | 149,111 |

| | 149,064 |

|

Credit facility | 123,000 |

| | 120,000 |

| | 125,000 |

| | 269,000 |

| | 215,000 |

|

Unsecured total | 1,016,424 |

| | 963,084 |

| | 869,063 |

| | 1,012,769 |

| | 958,475 |

|

Total | $ | 1,114,238 |

| | $ | 1,111,624 |

| | $ | 1,120,295 |

| | $ | 1,264,813 |

| | $ | 1,292,328 |

|

| | | | | | | | | |

Weighted Average Interest Rates | | | | | | | | | |

| | | | | | | | | |

Secured | | | | | | | | | |

Mortgage note payable, net | 4.5 | % | | 4.0 | % | | 5.3 | % | | 5.3 | % | | 5.4 | % |

Unsecured | | | | | | | | | |

Fixed rate bonds | 4.7 | % | | 4.7 | % | | 4.7 | % | | 4.7 | % | | 4.7 | % |

Term loans (1) | 2.8 | % | | 2.6 | % | | 2.7 | % | | 2.7 | % | | 2.7 | % |

Credit facility | 2.0 | % | | 1.6 | % | | 1.5 | % | | 1.4 | % | | 1.4 | % |

Unsecured total | 3.8 | % | | 3.8 | % | | 3.9 | % | | 3.6 | % | | 3.7 | % |

Weighted Average | 3.9 | % | | 3.8 | % | | 4.2 | % | | 3.9 | % | | 4.1 | % |

| | | | | | | | | |

(1) Washington REIT has entered into interest rate swaps to effectively fix the floating interest rates on its term loans (see page 10 of this Supplemental) |

| | | | | | | | | |

Note: The current debt balances outstanding are shown net of discounts, premiums and unamortized debt costs (see page 10 of this Supplemental). |

|

| |

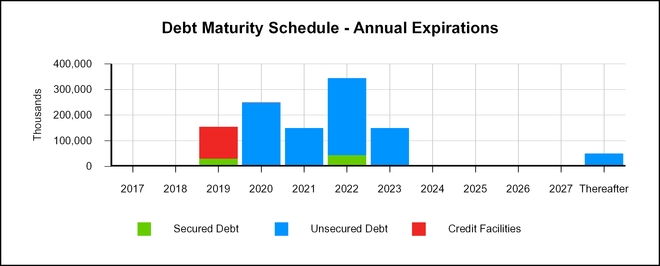

Long Term Debt Maturities (in thousands, except average interest rates) | |

|

| | | | | | | | | | | | | | | | | |

| Future Maturities of Debt |

Year | Secured Debt | | Unsecured Debt | | Credit Facilities | | Total Debt | | Avg Interest Rate |

2017 | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

| |

|

2018 | — |

| | — |

| | — |

| | — |

| |

|

2019 | 31,280 |

| | — |

| | 123,000 |

| (1) | 154,280 |

| | 2.7% |

2020 | — |

| | 250,000 |

| | — |

| | 250,000 |

| | 5.1% |

2021 | — |

| | 150,000 |

| (2) | — |

| | 150,000 |

| | 2.7% |

2022 | 44,517 |

| | 300,000 |

| | — |

| | 344,517 |

| | 4.0% |

2023 | — |

| | 150,000 |

| (3) | — |

| | 150,000 |

| | 2.8% |

2024 | — |

| | — |

| | — |

| | — |

| | |

2025 | — |

| | — |

| | — |

| | — |

| | |

2026 | — |

| | — |

| | — |

| | — |

| | |

2027 | — |

| | — |

| | — |

| | — |

| | |

Thereafter | — |

| | 50,000 |

| | — |

| | 50,000 |

| | 7.4% |

Scheduled principal payments | $ | 75,797 |

| | $ | 900,000 |

| | $ | 123,000 |

| | $ | 1,098,797 |

| | 3.9% |

Scheduled amortization payments | 18,342 |

| | — |

| | — |

| | 18,342 |

| | 4.8% |

Net discounts/premiums | 4,052 |

| | (1,873 | ) | | — |

| | 2,179 |

| | |

Loan costs, net of amortization | (377 | ) | | (4,703 | ) | | — |

| | (5,080 | ) | | |

Total maturities | $ | 97,814 |

| | $ | 893,424 |

| | $ | 123,000 |

| | $ | 1,114,238 |

| | 3.9% |

Weighted average maturity =4.8 years

(1) Maturity date for credit facility may be extended for up to two additional 6-month periods at Washington REIT's option.

(2) Washington REIT entered into an interest rate swap to effectively fix a LIBOR plus 110 basis points floating interest rate to a 2.72% all-in fixed interest rate commencing October 15, 2015.

(3) Washington REIT entered into interest rate swaps to effectively fix a LIBOR plus 165 basis points floating interest rate to a 2.86% all-in fixed interest rate commencing March 31, 2017.

|

| | | | | | | | | |

| Unsecured Notes Payable | | Unsecured Line of Credit

and Term Loans |

| Quarter Ended March 31, 2017 | | Covenant | | Quarter Ended March 31, 2017 | | Covenant |

% of Total Indebtedness to Total Assets(1) | 39.6 | % | | ≤ 65.0% | | N/A |

| | N/A |

Ratio of Income Available for Debt Service to Annual Debt Service | 3.9 |

| | ≥ 1.5 | | N/A |

| | N/A |

% of Secured Indebtedness to Total Assets(1) | 3.5 | % | | ≤ 40.0% | | N/A |

| | N/A |

Ratio of Total Unencumbered Assets(2) to Total Unsecured Indebtedness | 2.6 |

| | ≥ 1.5 | | N/A |

| | N/A |

% of Net Consolidated Total Indebtedness to Consolidated Total Asset Value(3) | N/A |

| | N/A | | 34.5 | % | | ≤ 60.0% |

Ratio of Consolidated Adjusted EBITDA(4) to Consolidated Fixed Charges(5) | N/A |

| | N/A | | 3.77 |

| | ≥ 1.50 |

% of Consolidated Secured Indebtedness to Consolidated Total Asset Value(3) | N/A |

| | N/A | | 3.1 | % | | ≤ 40.0% |

% of Consolidated Unsecured Indebtedness to Unencumbered Pool Value(6) | N/A |

| | N/A | | 33.5 | % | | ≤ 60.0% |

Ratio of Unencumbered Adjusted Net Operating Income to Consolidated Unsecured Interest Expense | N/A |

| | N/A | | 4.76 |

| | ≥ 1.75 |

| | | | | | | |

(1) Total Assets is calculated by applying a capitalization rate of 7.50% to the EBITDA(4) from the last four consecutive quarters, excluding EBITDA from acquired, disposed, and non-stabilized development properties. |

(2) Total Unencumbered Assets is calculated by applying a capitalization rate of 7.50% to the EBITDA(4) from unencumbered properties from the last four consecutive quarters, excluding EBITDA from acquired, disposed, and non-stabilized development properties. |

(3) Consolidated Total Asset Value is the sum of unrestricted cash plus the quotient of applying a capitalization rate to the annualized NOI from the most recently ended quarter for each asset class, excluding NOI from disposed properties, acquisitions during the past 6 quarters, development, major redevelopment and low occupancy properties. To this amount, we add the purchase price of acquisitions during the past 6 quarters plus values for development, major redevelopment and low occupancy properties. |

(4) Consolidated Adjusted EBITDA is defined as earnings before noncontrolling interests, depreciation, amortization, interest expense, income tax expense, acquisition costs, extraordinary, unusual or nonrecurring transactions including sale of assets, impairment, gains and losses on extinguishment of debt and other non-cash charges. |

(5) Consolidated Fixed Charges consist of interest expense excluding capitalized interest and amortization of deferred financing costs, principal payments and preferred dividends, if any. |

(6) Unencumbered Pool Value is the sum of unrestricted cash plus the quotient of applying a capitalization rate to the annualized NOI from unencumbered properties from the most recently ended quarter for each asset class excluding NOI from disposed properties, acquisitions during the past 6 quarters, development, major redevelopment and low occupancy properties. To this we add the purchase price of unencumbered acquisitions during the past 6 quarters and values for unencumbered development, major redevelopment and low occupancy properties. |

|

| |

Capital Analysis (In thousands, except per share amounts) | |

|

| | | | | | | | | | | | | | | | | | | |

| Three Months Ended |

| 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Market Data | | | | | | | | | |

| | | | | | | | | |

Shares Outstanding | $ | 75,702 |

| | $ | 74,606 |

| | $ | 74,579 |

| | $ | 73,651 |

| | $ | 68,326 |

|

Market Price per Share | 31.28 |

| | 32.69 |

| | 31.12 |

| | 31.46 |

| | 29.21 |

|

Equity Market Capitalization | $ | 2,367,959 |

| | $ | 2,438,870 |

| | $ | 2,320,898 |

| | $ | 2,317,060 |

| | $ | 1,995,802 |

|

| | | | | | | | | |

Total Debt | $ | 1,114,238 |

| | $ | 1,111,624 |

| | $ | 1,120,295 |

| | $ | 1,264,813 |

| | $ | 1,292,328 |

|

Total Market Capitalization | $ | 3,482,197 |

| | $ | 3,550,494 |

| | $ | 3,441,193 |

| | $ | 3,581,873 |

| | $ | 3,288,130 |

|

| | | | | | | | | |

Total Debt to Market Capitalization | 0.32 | :1 | | 0.31 | :1 | | 0.33 | :1 | | 0.35 | :1 | | 0.39 | :1 |

| | | | | | | | | |

Earnings to Fixed Charges(1) | 1.6x |

| | 1.4x |

| | 6.9x |

| | 3.3x |

| | 1.2x |

|

Debt Service Coverage Ratio(2) | 3.6x |

| | 3.4x |

| | 3.3x |

| | 3.2x |

| | 2.8x |

|

| | | | | | | | | |

Dividend Data | Three Months Ended |

| 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Total Dividends Declared | $ | 22,607 |

| | $ | 22,414 |

| | $ | 22,365 |

| | $ | 22,147 |

| | $ | 20,644 |

|

Common Dividend Declared per Share | $ | 0.30 |

| | $ | 0.30 |

| | $ | 0.30 |

| | $ | 0.30 |

| | $ | 0.30 |

|

| | | | | | | | | |

(1) The ratio of earnings to fixed charges is computed by dividing earnings by fixed charges. For this purpose, earnings consist of income from continuing operations attributable to the controlling interests plus fixed charges, less capitalized interest. Fixed charges consist of interest expense, including amortized costs of debt issuance, plus interest costs capitalized. The earnings to fixed charges ratios for the three months ended September 30, 2016 and June 30, 2016 include gains on the sale of real estate of $77.6 million and $24.1 million, respectively. |

(2) Debt service coverage ratio is computed by dividing Adjusted EBITDA (see page 8) by interest expense and principal amortization. |

|

| |

Same-Store Portfolio Net Operating Income (NOI) Growth & Rental Rate Growth 2016 vs. 2015 | |

|

| | | | | | | | | | | | | |

| Three Months Ended March 31, | | | | Rental Rate |

| 2017 | | 2016 | | % Change | | Growth |

Cash Basis: | | | | | | | |

Multifamily | $ | 11,116 |

| | $ | 10,698 |

| | 3.9 | % | | 1.2 | % |

Office | 21,474 |

| | 18,651 |

| | 15.1 | % | | 0.5 | % |

Retail | 11,508 |

| | 10,653 |

| | 8.0 | % | | 0.5 | % |

Overall Same-Store Portfolio (1) | $ | 44,098 |

| | $ | 40,002 |

| | 10.2 | % | | 0.7 | % |

| | | | | | | |

GAAP Basis: | | | | | | | |

Multifamily | $ | 11,112 |

| | $ | 10,686 |

| | 4.0 | % | | 1.3 | % |

Office | 21,311 |

| | 18,443 |

| | 15.6 | % | | 1.0 | % |

Retail | 11,842 |

| | 10,974 |

| | 7.9 | % | | 0.6 | % |

Overall Same-Store Portfolio (1) | $ | 44,265 |

| | $ | 40,103 |

| | 10.4 | % | | 1.0 | % |

|

|

(1) Non same-store properties were: |

Acquisitions: |

Multifamily - Riverside Apartments |

Development/Redevelopment: |

Office - The Army Navy Building and Braddock Metro Center |

Sold properties: |

Office - Dulles Station II, Wayne Plaza, 600 Jefferson Plaza, 6110 Executive Boulevard, West Gude, 51 Monroe Street and One Central Plaza |

|

| |

Same-Store Portfolio Net Operating Income (NOI) Detail (In thousands) | |

|

| | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, 2017 |

| Multifamily | | Office | | Retail | | Corporate and Other | | Total |

Real estate rental revenue | | | | | | | | | |

Same-store portfolio | $ | 18,256 |

| | $ | 34,082 |

| | $ | 15,705 |

| | $ | — |

| | $ | 68,043 |

|

Non same-store - acquired and in development (1) | 5,513 |

| | 3,945 |

| | — |

| | — |

| | 9,458 |

|

Total | 23,769 |

| | 38,027 |

| | 15,705 |

| | — |

| | 77,501 |

|

Real estate expenses | | | | | | | | | |

Same-store portfolio | 7,144 |

| | 12,771 |

| | 3,863 |

| | — |

| | 23,778 |

|

Non same-store - acquired and in development (1) | 2,442 |

| | 1,643 |

| | — |

| | — |

| | 4,085 |

|

Total | 9,586 |

| | 14,414 |

| | 3,863 |

| | — |

| | 27,863 |

|

Net Operating Income (NOI) | | | | | | | | | |

Same-store portfolio | 11,112 |

| | 21,311 |

| | 11,842 |

| | — |

| | 44,265 |

|

Non same-store - acquired and in development (1) | 3,071 |

| | 2,302 |

| | — |

| | — |

| | 5,373 |

|

Total | $ | 14,183 |

| | $ | 23,613 |

| | $ | 11,842 |

| | $ | — |

| | $ | 49,638 |

|

| | | | | | | | | |

Same-store portfolio NOI (from above) | $ | 11,112 |

| | $ | 21,311 |

| | $ | 11,842 |

| | $ | — |

| | $ | 44,265 |

|

Straight-line revenue, net for same-store properties | 3 |

| | (617 | ) | | (156 | ) | | — |

| | (770 | ) |

FAS 141 Min Rent | 1 |

| | 49 |

| | (227 | ) | | — |

| | (177 | ) |

Amortization of lease intangibles for same-store properties | — |

| | 731 |

| | 49 |

| | — |

| | 780 |

|

Same-store portfolio cash NOI | $ | 11,116 |

| | $ | 21,474 |

| | $ | 11,508 |

| | $ | — |

| | $ | 44,098 |

|

Reconciliation of NOI to net income | | | | | | | | | |

Total NOI | $ | 14,183 |

| | $ | 23,613 |

| | $ | 11,842 |

| | $ | — |

| | $ | 49,638 |

|

Depreciation and amortization | (7,490 | ) | | (14,672 | ) | | (3,707 | ) | | (200 | ) | | (26,069 | ) |

General and administrative | — |

| | — |

| | — |

| | (5,626 | ) | | (5,626 | ) |

Interest expense | (978 | ) | | (148 | ) | | (194 | ) | | (10,085 | ) | | (11,405 | ) |

Other income | — |

| | — |

| | — |

| | 77 |

| | 77 |

|

Net income (loss) | 5,715 |

| | 8,793 |

| | 7,941 |

| | (15,834 | ) | | 6,615 |

|

Net loss attributable to noncontrolling interests | — |

| | — |

| | — |

| | 19 |

| | 19 |

|

Net income (loss) attributable to the controlling interests | $ | 5,715 |

| | $ | 8,793 |

| | $ | 7,941 |

| | $ | (15,815 | ) | | $ | 6,634 |

|

(1) For a list of non-same-store properties and held for sale and sold properties, see page 13 of this Supplemental. | | |

|

| |

Same-Store Net Operating Income (NOI) Detail (In thousands) | |

|

| | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, 2016 |

| Multifamily | | Office | | Retail | | Corporate and Other | | Total |

Real estate rental revenue | | | | | | | | | |

Same-store portfolio | $ | 17,939 |

| | $ | 30,732 |

| | $ | 15,380 |

| | $ | — |

| | $ | 64,051 |

|

Non same-store - acquired and in development (1) | — |

| | 13,086 |

| | — |

| | — |

| | 13,086 |

|

Total | 17,939 |

| | 43,818 |

| | 15,380 |

| | — |

| | 77,137 |

|

| | | | | | | | | |

Real estate expenses | | | | | | | | | |

Same-store portfolio | 7,253 |

| | 12,289 |

| | 4,406 |

| | — |

| | 23,948 |

|

Non same-store - acquired and in development (1) | — |

| | 4,786 |

| |

|

| | — |

| | 4,786 |

|

Total | 7,253 |

| | 17,075 |

| | 4,406 |

| | — |

| | 28,734 |

|

| | | | | | | | | |

Net Operating Income (NOI) | | | | | | | | | |

Same-store portfolio | 10,686 |

| | 18,443 |

| | 10,974 |

| | — |

| | 40,103 |

|

Non same-store - acquired and in development (1) | — |

| | 8,300 |

| | — |

| | — |

| | 8,300 |

|

Total | $ | 10,686 |

| | $ | 26,743 |

| | $ | 10,974 |

| | $ | — |

| | $ | 48,403 |

|

| | | | | | | | | |

Same-store portfolio NOI (from above) | $ | 10,686 |

| | $ | 18,443 |

| | $ | 10,974 |

| | $ | — |

| | $ | 40,103 |

|

Straight-line revenue, net for same-store properties | 11 |

| | (490 | ) | | (116 | ) | | — |

| | (595 | ) |

FAS 141 Min Rent | 1 |

| | 113 |

| | (254 | ) | | — |

| | (140 | ) |

Amortization of lease intangibles for same-store properties | — |

| | 585 |

| | 49 |

| | — |

| | 634 |

|

Same-store portfolio cash NOI | $ | 10,698 |

| | $ | 18,651 |

| | $ | 10,653 |

| | $ | — |

| | $ | 40,002 |

|

| | | | | | | | | |

Reconciliation of NOI to net income | | | | | | | | | |

Total NOI | $ | 10,686 |

| | $ | 26,743 |

| | $ | 10,974 |

| | $ | — |

| | $ | 48,403 |

|

Depreciation and amortization | (5,403 | ) | | (16,783 | ) | | (3,609 | ) | | (243 | ) | | (26,038 | ) |

General and administrative | — |

| | — |

| | — |

| | (5,511 | ) | | (5,511 | ) |

Interest expense | (2,243 | ) | | (2,527 | ) | | (216 | ) | | (9,374 | ) | | (14,360 | ) |

Other income | — |

| | — |

| | — |

| | 39 |

| | 39 |

|

Acquisition costs | — |

| | — |

| | — |

| | (154 | ) | | (154 | ) |

Net income (loss) | 3,040 |

| | 7,433 |

| | 7,149 |

| | (15,243 | ) | | 2,379 |

|

Net income attributable to noncontrolling interests | — |

| | — |

| | — |

| | 5 |

| | 5 |

|

Net income (loss) attributable to the controlling interests | $ | 3,040 |

| | $ | 7,433 |

| | $ | 7,149 |

| | $ | (15,238 | ) | | $ | 2,384 |

|

(1) For a list of non-same-store properties and held for sale and sold properties, see page 13 of this Supplemental. | | |

|

| |

Net Operating Income (NOI) by Region | |

|

| | | | | |

| | | | |

| | Percentage of NOI | | |

| | Q1 2017 | | |

| DC | | | |

| Multifamily | 5.9 | % | | |

| Office | 24.1 | % | | |

| Retail | 1.9 | % | | |

| | 31.9 | % | | |

| Maryland | | | |

| Multifamily | 2.3 | % | | |

| Retail | 14.4 | % | | |

| | 16.7 | % | | |

| Virginia | | | |

| Multifamily | 20.3 | % | | |

| Office | 23.5 | % | | |

| Retail | 7.6 | % | | |

| | 51.4 | % | | |

| | | | |

| Total Portfolio | 100.0 | % | | |

|

| | | | |

Same-Store Portfolio and Overall Ending Occupancy Levels by Sector

| |

|

| | | | | | | | | | | | | | | |

| | Ending Occupancy - Same-Store Properties (1), (2) |

Sector | | 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Multifamily (calculated on a unit basis) | | 94.8 | % | | 95.6 | % | | 92.4 | % | | 94.6 | % | | 95.2 | % |

| | | | | | | | | | |

Multifamily | | 94.2 | % | | 95.2 | % | | 94.8 | % | | 94.2 | % | | 94.5 | % |

Office | | 93.1 | % | | 91.7 | % | | 91.0 | % | | 86.9 | % | | 86.3 | % |

Retail | | 93.8 | % | | 95.7 | % | | 95.6 | % | | 92.1 | % | | 91.2 | % |

| | | | | | | | | | |

Overall Portfolio | | 93.7 | % | | 94.0 | % | | 93.6 | % | | 90.8 | % | | 90.5 | % |

| | | | | | | | | | |

| | Ending Occupancy - All Properties (2) |

Sector | | 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Multifamily (calculated on a unit basis) | | 94.6 | % | | 94.7 | % | | 94.5 | % | | 94.7 | % | | 95.2 | % |

| | | | | | | | | | |

Multifamily | | 94.2 | % | | 94.5 | % | | 94.2 | % | | 94.4 | % | | 94.5 | % |

Office | | 92.4 | % | | 91.1 | % | | 90.5 | % | | 87.5 | % | | 87.8 | % |

Retail | | 93.8 | % | | 95.7 | % | | 95.6 | % | | 92.1 | % | | 91.2 | % |

| | | | | | | | | | |

Overall Portfolio | | 93.5 | % | | 93.5 | % | | 93.2 | % | | 91.1 | % | | 90.6 | % |

|

|

(1) Non same-store properties were: |

Acquisitions: |

Multifamily - Riverside Apartments |

Development/Redevelopment: |

Office - The Army Navy Building and Braddock Metro Center |

Sold properties: |

Office - Wayne Plaza, 600 Jefferson Plaza, 6110 Executive Boulevard, West Gude, 51 Monroe Street and One Central Plaza |

|

(2) Ending occupancy is calculated as occupied square footage as a percentage of total square footage as of the last day of that period, except for the rows labeled "Multifamily (calculated on a unit basis)," on which ending occupancy is calculated as occupied units as a percentage of total available units as of the last day of that period. |

|

| | | | |

Same-Store Portfolio and Overall Economic Occupancy Levels by Sector | |

|

| | | | | | | | | | | | | | | |

| | Economic Occupancy - Same-Store Properties(1) |

Sector | | 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Multifamily | | 94.8 | % | | 95.1 | % | | 95.2 | % | | 95.0 | % | | 93.9 | % |

Office | | 93.6 | % | | 91.9 | % | | 89.9 | % | | 85.7 | % | | 84.5 | % |

Retail | | 92.1 | % | | 93.6 | % | | 91.8 | % | | 89.3 | % | | 89.7 | % |

| | | | | | | | | | |

Overall Portfolio | | 93.6 | % | | 93.2 | % | | 91.8 | % | | 89.0 | % | | 88.2 | % |

| | | | | | | | | | |

| | Economic Occupancy - All Properties |

Sector | | 3/31/2017 | | 12/31/2016 | | 9/30/2016 | | 6/30/2016 | | 3/31/2016 |

Multifamily | | 94.0 | % | | 94.4 | % | | 94.6 | % | | 95.3 | % | | 93.9 | % |

Office | | 92.0 | % | | 91.1 | % | | 89.5 | % | | 86.6 | % | | 86.9 | % |

Retail | | 92.1 | % | | 93.6 | % | | 91.8 | % | | 89.3 | % | | 89.7 | % |

| | | | | | | | | | |

Overall Portfolio | | 92.7 | % | | 92.6 | % | | 91.5 | % | | 89.3 | % | | 89.0 | % |

|

|

(1) Non same-store properties were: |

Acquisitions: |

Multifamily - Riverside Apartments |

Development/Redevelopment: |

Office - The Army Navy Building and Braddock Metro Center |

Sold properties: |

Office - Wayne Plaza, 600 Jefferson Plaza, 6110 Executive Boulevard, West Gude, 51 Monroe Street and One Central Plaza |

|

| | | | |

Development/Re-development Summary

| |

|

| | | | | | | | | |

Property and Location | Total Rentable Square Feet or # of Units | Anticipated Total Cash Cost (1) (in thousands) | Cash Cost to Date (1) (in thousands) | Anticipated Construction Completion Date | Leased % as of 3/31/2017 |

Development Summary | | | | | |

Trove (Wellington land parcel), Arlington, VA | 401 units | $ | 122,252 |

| $ | 18,911 |

| third quarter 2019 (2) | N/A |

| | | | | |

Re-development Summary | | | | | |

The Army Navy Building (3), Washington DC | 108,000 square feet | $ | 4,045 |

| $ | 2,203 |

| second quarter 2017 | 55% |

Spring Valley Village, Washington DC | 14,000 additional square feet | $ | 4,496 |

| $ | 887 |

| fourth quarter 2017 | N/A |

(1) Represents anticipated/actual cash expenditures, and excludes allocations of capitalized corporate overhead costs and interest.

(2) This development project has two phases: Phase I consists of two buildings totaling 226 units and a garage, with delivery of units anticipated to commence in third quarter 2019; Phase II consists of one building with 175 units, anticipated to commence in third quarter 2020.

(3) This re-development project primarily consists of adding amenities, to include a lounge and conference center with access to the rooftop and a renovated penthouse, and upgrading the building's lobby and other common areas.

|

| |

Commercial Leasing Summary - New Leases

| |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 1st Quarter 2017 | | 4th Quarter 2016 | | 3rd Quarter 2016 | | 2nd Quarter 2016 | | 1st Quarter 2016 |

Gross Leasing Square Footage | | | | | | | | | | | | | | | | | | | |

Office Buildings | 36,102 | | | 39,047 | | | 60,538 | | | 28,154 | | | 32,249 | |

Retail Centers | 8,355 | | | 10,362 | | | 1,342 | | | 6,313 | | | 11,777 | |

Total | 44,457 | |

| 49,409 | |

| 61,880 | | | 34,467 | | | 44,026 | |

Weighted Average Term (years) | | | | | | | | | | | | | | | | | | | |

Office Buildings | 8.5 | | | 4.9 | | | 6.4 | | | 6.1 | | | 7.7 | |

Retail Centers | 6.2 | | | 9.2 | | | 8.3 | | | 8.0 | | | 9.8 | |

Total | 8.1 | | | 5.8 | | | 6.4 | | | 6.5 | | | 8.3 | |

Weighted Average Free Rent Period (months) (1) | | | | | | | | | | | | | | | | |

Office Buildings | 9.1 | | | 3.0 | | | 6.1 | | | 5.9 | | | 7.5 | |

Retail Centers | 2.7 | | | 1.0 | | | 3.9 | | | 1.2 | | | 7.6 | |

Total | 8.0 | | | 2.5 | | | 6.1 | | | 5.3 | | | 7.5 | |

| | | | | | | | | | | | | | | | | | | |

Rental Rate Increases: | GAAP | | CASH | | GAAP | | CASH | | GAAP | | CASH | | GAAP | | CASH | | GAAP | | CASH |

Rate on expiring leases | | | | | | | | | | | | | | | | | | | |

Office Buildings | $ | 32.50 |

| | $ | 33.83 |

| | $ | 40.36 |

| | $ | 42.92 |

| | $ | 39.31 |

| | $ | 39.01 |

| | $ | 34.80 |

| | $ | 35.43 |

| | $ | 30.91 |

| | $ | 31.78 |

|

Retail Centers | 37.15 |

| | 35.16 |

| | 38.26 |

| | 38.99 |

| | 43.67 |

| | 46.15 |

| | 28.92 |

| | 29.11 |

| | 11.93 |

| | 12.04 |

|

Total | $ | 33.37 |

| | $ | 34.08 |

| | $ | 39.92 |

| | $ | 42.10 |

| | $ | 39.40 |

| | $ | 39.17 |

| | $ | 33.73 |

| | $ | 34.27 |

| | $ | 25.83 |

| | $ | 26.50 |

|

| | | | | | | | | | | | | | | | | | | |

Rate on new leases | | | | | | | | | | | | | | | | | | | |

Office Buildings | $ | 43.20 |

| | $ | 38.67 |

| | $ | 42.64 |

| | $ | 39.96 |

| | $ | 44.06 |

| | $ | 40.80 |

| | $ | 39.83 |

| | $ | 37.09 |

| | $ | 40.60 |

| | $ | 36.84 |

|

Retail Centers | 36.39 |

| | 34.46 |

| | 44.14 |

| | 40.37 |

| | 60.89 |

| | 55.00 |

| | 28.13 |

| | 26.45 |

| | 16.22 |

| | 14.45 |

|

Total | $ | 41.92 |

| | $ | 37.88 |

| | $ | 42.96 |

| | $ | 40.05 |

| | $ | 44.42 |

| | $ | 41.10 |

| | $ | 37.69 |

| | $ | 35.14 |

| | $ | 34.08 |

| | $ | 30.85 |

|

| | | | | | | | | | | | | | | | | | | |

Percentage Increase | | | | | | | | | | | | | | | | | | | |

Office Buildings | 33.0 | % | | 14.3 | % | | 5.7 | % | | (6.9 | )% | | 12.1 | % | | 4.6 | % | | 14.5 | % | | 4.7 | % | | 31.4 | % | | 15.9 | % |

Retail Centers | (2.1 | )% | | (2.0 | )% | | 15.4 | % | | 3.5 | % | | 39.4 | % | | 19.2 | % | | (2.7 | )% | | (9.1 | )% | | 35.9 | % | | 20.0 | % |

Total | 25.6 | % | | 11.1 | % | | 7.6 | % | | (4.9 | )% | | 12.7 | % | | 4.9 | % | | 11.8 | % | | 2.5 | % | | 31.9 | % | | 16.4 | % |

| | | | | | | | | | | | | | | | | | | |

| Total Dollars | | $ per Sq Ft | | Total Dollars | | $ per Sq Ft | | Total Dollars | | $ per Sq Ft | | Total Dollars | | $ per Sq Ft | | Total Dollars | | $ per Sq Ft |

Tenant Improvements | | | | | | | | | | | | | | | | | | | |

Office Buildings | $ | 2,333,378 |

| | $ | 64.63 |

| | $ | 1,244,745 |

| | $ | 31.88 |

| | $ | 2,682,882 |

| | $ | 44.32 |

| | $ | 1,356,810 |

| | $ | 48.19 |

| | $ | 1,571,632 |

| | $ | 48.73 |

|

Retail Centers | 60,030 |

| | 7.18 |

| | 307,953 |

| | 29.72 |

| | — |

| | — |

| | 111,840 |

| | 17.72 |

| | 203,276 |

| | 17.26 |

|

Subtotal | $ | 2,393,408 |

| | $ | 53.84 |

| | $ | 1,552,698 |

| | $ | 31.43 |

| | $ | 2,682,882 |

| | $ | 43.36 |

| | $ | 1,468,650 |

| | $ | 42.61 |

| | $ | 1,774,908 |

| | $ | 40.31 |

|

Leasing Commissions (1) | | | | | | | | | | | | | | | | |

Office Buildings | $ | 688,811 |

| | $ | 19.08 |

| | $ | 424,951 |

| | $ | 10.88 |

| | $ | 890,195 |

| | $ | 14.70 |

| | $ | 375,882 |

| | $ | 13.35 |

| | $ | 505,349 |

| | $ | 15.67 |

|

Retail Centers | 98,930 |

| | 11.84 |

| | 212,162 |

| | 20.48 |

| | 39,380 |

| | 29.34 |

| | 80,461 |

| | 12.75 |

| | 103,983 |

| | 8.83 |

|

Subtotal | $ | 787,741 |

| | $ | 17.72 |

| | $ | 637,113 |

| | $ | 12.89 |

| | $ | 929,575 |

| | $ | 15.02 |

| | $ | 456,343 |

| | $ | 13.24 |

| | $ | 609,332 |

| | $ | 13.84 |

|

Tenant Improvements and Leasing Commissions | | | | | | | | | | |

Office Buildings | $ | 3,022,189 |

| | $ | 83.71 |

| | $ | 1,669,696 |

| | $ | 42.76 |

| | $ | 3,573,077 |

| | $ | 59.02 |

| | $ | 1,732,692 |

| | $ | 61.54 |

| | $ | 2,076,981 |

| | $ | 64.40 |

|

Retail Centers | 158,960 |

| | 19.02 |

| | 520,115 |

| | 50.20 |

| | 39,380 |

| | 29.34 |

| | 192,301 |

| | 30.47 |

| | 307,259 |

| | 26.09 |

|

Total | $ | 3,181,149 |

| | $ | 71.56 |

| | $ | 2,189,811 |

| | $ | 44.32 |

| | $ | 3,612,457 |

| | $ | 58.38 |

| | $ | 1,924,993 |

| | $ | 55.85 |

| | $ | 2,384,240 |

| | $ | 54.15 |

|

|

| |

Commercial Leasing Summary - Renewal Leases | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 1st Quarter 2017 | | 4th Quarter 2016 | | 3rd Quarter 2016 | | 2nd Quarter 2016 | | 1st Quarter 2016 |

Gross Leasing Square Footage | | | | | | | | | | | | | | | | | | | |

Office Buildings | 104,283 | | | 64,956 | | | 151,722 | | | 30,787 | | | 193,275 | |

Retail Centers | 47,279 | | | 65,934 | | | 74,535 | | | 9,076 | | | 27,243 | |

Total | 151,562 | | | 130,890 | | | 226,257 | | | 39,863 | | | 220,518 | |

Weighted Average Term (years) | | | | | | | | | | | | | | | | | | | |

Office Buildings | 11.8 | | | 4.9 | | | 3.7 | | | 4.6 | | | 7.1 | |

Retail Centers | 5.7 | | | 4.9 | | | 4.7 | | | 6.3 | | | 11.6 | |

Total | 9.9 | | | 4.9 | | | 4.0 | | | 5.0 | | | 7.6 | |

Weighted Average Free Rent Period (months) (1) | | | | | | | | | | | | | | | | |

Office Buildings | 12.1 | | | 3.1 | | | 2.4 | | | 4.4 | | | 7.9 | |

Retail Centers | — | | | — | | | — | | | 0.7 | | | 5.1 | |

Total | 9.1 | | | 1.8 | | | 1.8 | | | 3.3 | | | 7.5 | |

| | | | | | | | | | | | | | | | | | | |

Rental Rate Increases: | GAAP | | CASH | | GAAP | | CASH | | GAAP | | CASH | | GAAP | | CASH | | GAAP | | CASH |

Rate on expiring leases | | | | | | | | | | | | | | | | | | | |

Office Buildings | $ | 46.52 |

| | $ | 50.00 |

| | $ | 43.31 |

| | $ | 43.62 |

| | $ | 35.85 |

| | $ | 36.37 |

| | $ | 30.13 |

| | $ | 31.53 |

| | $ | 36.53 |

| | $ | 38.93 |

|

Retail Centers | 32.13 |

| | 33.61 |

| | 27.52 |

| | 27.66 |

| | 25.03 |

| | 25.28 |

| | 32.56 |

| | 47.14 |

| | 24.53 |

| | 26.67 |

|

Total | $ | 42.03 |

| | $ | 44.88 |

| | $ | 35.36 |

| | $ | 35.58 |

| | $ | 32.28 |

| | $ | 32.72 |

| | $ | 30.69 |

| | $ | 35.08 |

| | $ | 35.04 |

| | $ | 37.42 |

|

| | | | | | | | | | | | | | | | | | | |

Rate on new leases | | | | | | | | | | | | | | | | | | | |

Office Buildings | $ | 58.13 |

| | $ | 50.05 |

| | $ | 46.84 |

| | $ | 44.18 |

| | $ | 42.20 |

| | $ | 40.38 |

| | $ | 34.42 |

| | $ | 32.44 |

| | $ | 40.55 |

| | $ | 37.12 |

|

Retail Centers | 37.10 |

| | 35.64 |

| | 30.27 |

| | 29.81 |

| | 27.61 |

| | 26.58 |

| | 41.78 |

| | 46.62 |

| | 41.49 |

| | 35.39 |

|

Total | $ | 51.57 |

| | $ | 45.56 |

| | $ | 38.49 |

| | $ | 36.94 |

| | $ | 37.39 |

| | $ | 35.84 |

| | $ | 36.10 |

| | $ | 35.67 |

| | $ | 40.66 |

| | $ | 36.90 |

|

| | | | | | | | | | | | | | | | | | | |

Percentage Increase | | | | | | | | | | | | | | | | | | | |

Office Buildings | 25.0 | % | | 0.1 | % | | 8.1 | % | | 1.3 | % | | 17.7 | % | | 11.0 | % | | 14.2 | % | | 2.9 | % | | 11.0 | % | | (4.7 | )% |

Retail Centers | 15.5 | % | | 6.0 | % | | 10.0 | % | | 7.8 | % | | 10.3 | % | | 5.1 | % | | 28.3 | % | | (1.1 | )% | | 69.2 | % | | 32.7 | % |

Total | 22.7 | % | | 1.5 | % | | 8.9 | % | | 3.8 | % | | 15.8 | % | | 9.5 | % | | 17.6 | % | | 1.7 | % | | 16.0 | % | | (1.4 | )% |

| | | | | | | | | | | | | | | | | | | |

| Total Dollars | | $ per Sq Ft | | Total Dollars | | $ per Sq Ft | | Total Dollars | | $ per Sq Ft | | Total Dollars | | $ per Sq Ft | | Total Dollars | | $ per Sq Ft |

Tenant Improvements | | | | | | | | | | | | | | | | | | | |

Office Buildings | $ | 9,703,224 |

| | $ | 93.05 |

| | $ | 1,068,629 |

| | $ | 16.45 |

| | $ | 2,243,523 |

| | $ | 14.79 |

| | $ | 153,365 |

| | $ | 4.98 |

| | $ | 6,945,781 |

| | $ | 35.94 |

|

Retail Centers | 111,925 |

| | 2.37 |

| | 56,940 |

| | 0.86 |

| | — |

| | — |

| | — |

| | — |

| | 626,200 |

| | 22.99 |

|

Subtotal | $ | 9,815,149 |

| | $ | 64.76 |

| | $ | 1,125,569 |

| | $ | 8.60 |

| | $ | 2,243,523 |

| | $ | 9.92 |

| | $ | 153,365 |

| | $ | 3.85 |

| | $ | 7,571,981 |

| | $ | 34.34 |

|

Leasing Commissions (1) | | | | | | | | | | | | | | | | | | |

Office Buildings | $ | 2,981,750 |

| | $ | 28.59 |

| | $ | 735,713 |

| | $ | 11.33 |

| | $ | 780,080 |

| | $ | 5.14 |

| | $ | 198,223 |

| | $ | 6.44 |

| | $ | 2,801,717 |

| | $ | 14.50 |

|

Retail Centers | 137,765 |

| | 2.91 |

| | 120,858 |

| | 1.83 |

| | 124,121 |

| | 1.67 |

| | 74,824 |

| | 8.24 |

| | 394,380 |

| | 14.48 |

|

Subtotal | $ | 3,119,515 |

| | $ | 20.58 |

| | $ | 856,571 |

| | $ | 6.54 |

| | $ | 904,201 |

| | $ | 4.00 |

| | $ | 273,047 |

| | $ | 6.85 |

| | $ | 3,196,097 |

| | $ | 14.49 |

|

Tenant Improvements and Leasing Commissions | | | | | | | | | | |

Office Buildings | $ | 12,684,974 |

| | $ | 121.64 |

| | $ | 1,804,342 |

| | $ | 27.78 |

| | $ | 3,023,603 |

| | $ | 19.93 |

| | $ | 351,588 |

| | $ | 11.42 |

| | $ | 9,747,498 |

| | $ | 50.44 |

|

Retail Centers | 249,690 |

| | 5.28 |

| | 177,798 |

| | 2.69 |

| | 124,121 |

| | 1.67 |

| | 74,824 |

| | 8.24 |

| | 1,020,580 |

| | 37.47 |

|

Total | $ | 12,934,664 |

| | $ | 85.34 |

| | $ | 1,982,140 |

| | $ | 15.14 |

| | $ | 3,147,724 |

| | $ | 13.92 |

| | $ | 426,412 |

| | $ | 10.70 |

| | $ | 10,768,078 |

| | $ | 48.83 |

|

|

| |

10 Largest Tenants - Based on Annualized Commercial Income | |

March 31, 2017 |

|

| | | | | | | | | | | | | |

Tenant | Number of Buildings | | Weighted Average Remaining Lease Term in Months | | Percentage of Aggregate Portfolio Annualized Commercial Income | | Aggregate Rentable Square Feet | | Percentage of Aggregate Occupied Square Feet |

World Bank | 1 | | 45 |

| | 6.10 | % | | 210,354 |

| | 3.80 | % |

Advisory Board Company | 2 | | 26 |

| | 4.02 | % | | 199,762 |

| | 3.61 | % |

Capital One | 5 | | 57 |

| | 3.23 | % | | 148,742 |

| | 2.69 | % |

Engility Corporation | 1 | | 6 |

| | 2.88 | % | | 134,126 |

| | 2.43 | % |

Squire Patton Boggs (USA) LLP (1) | 1 | | 1 |

| | 2.70 | % | | 110,566 |

| | 2.00 | % |

Booz Allen Hamilton, Inc. | 1 | | 106 |

| | 2.57 | % | | 222,989 |

| | 4.03 | % |

Epstein, Becker & Green, P.C. | 1 | | 129 |

| | 1.66 | % | | 60,544 |

| | 1.10 | % |

Hughes Hubbard & Reed LLP | 1 | | 171 |

| | 1.64 | % | | 54,154 |

| | 0.98 | % |

Alexandria City School Board | 1 | | 146 |

| | 1.32 | % | | 84,693 |

| | 1.53 | % |

Morgan Stanley Smith Barney Financing | 1 | | 47 |

| | 1.15 | % | | 49,395 |

| | 0.89 | % |

Total/Weighted Average | | | 62 |

| | 27.27 | % | | 1,275,325 |

| | 23.06 | % |

(1) The spaced leased to Squire Patton Boggs (USA) LLP is currently subleased to Advisory Board Company, who has signed an extension to make the lease coterminous with the remaining Advisory Board Company leases expiring on May 31, 2019.

|

| |

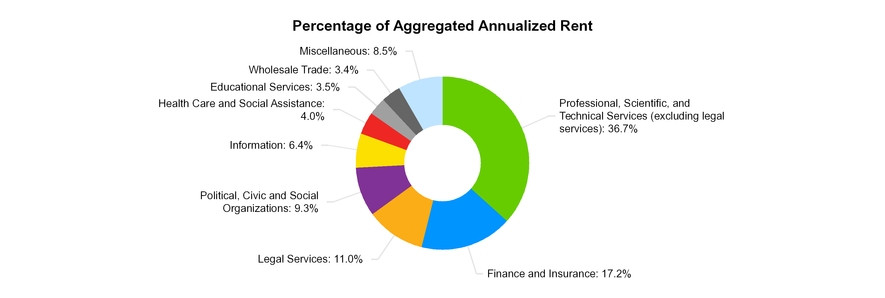

Industry Diversification - Office | |

March 31, 2017 |

|

| | | | | | | | | | | | |

Industry Classification (NAICS) | Annualized Base Rental Revenue | | Percentage of Aggregate Annualized Rent | | Aggregate Rentable Square Feet | | Percentage of Aggregate Square Feet |

Office: | | | | | | | |

Professional, Scientific, and Technical Services (excluding legal services) | $ | 48,483,617 |

| | 36.73 | % | | 1,386,687 |

| | 41.03 | % |

Finance and Insurance | 22,706,665 |

| | 17.20 | % | | 487,270 |

| | 14.42 | % |

Legal Services | 14,546,311 |

| | 11.02 | % | | 316,601 |

| | 9.37 | % |

Political, Civic and Social Organizations | 12,289,870 |

| | 9.31 | % | | 303,565 |

| | 8.98 | % |

Information | 8,501,846 |

| | 6.44 | % | | 195,413 |

| | 5.78 | % |

Health Care and Social Assistance | 5,239,756 |

| | 3.97 | % | | 153,448 |

| | 4.54 | % |

Educational Services | 4,622,502 |

| | 3.50 | % | | 144,870 |

| | 4.29 | % |

Wholesale Trade | 4,517,830 |

| | 3.42 | % | | 103,177 |

| | 3.05 | % |

Miscellaneous: | | | | | | | |

Administrative and Support and Waste Management and Remediation Services | 2,964,591 |

| | 2.25 | % | | 68,960 |

| | 2.04 | % |

Real Estate and Rental and Leasing | 1,770,715 |

| | 1.34 | % | | 42,052 |

| | 1.24 | % |

Accommodation and Food Services | 1,731,972 |

| | 1.31 | % | | 43,599 |

| | 1.29 | % |

Public Administration | 1,646,056 |

| | 1.25 | % | | 45,928 |

| | 1.36 | % |

Other | 2,980,284 |

| | 2.26 | % | | 88,191 |

| | 2.61 | % |

Total | $ | 132,002,015 |

| | 100.00 | % | | 3,379,761 |

| | 100.00 | % |

Note: Federal government tenants comprise less than 1.0% of annualized base rental revenue. | | | | | | | |

|

|

Industry Diversification - Retail |

March 31, 2017 |

|

| | | | | | | | | | | | |

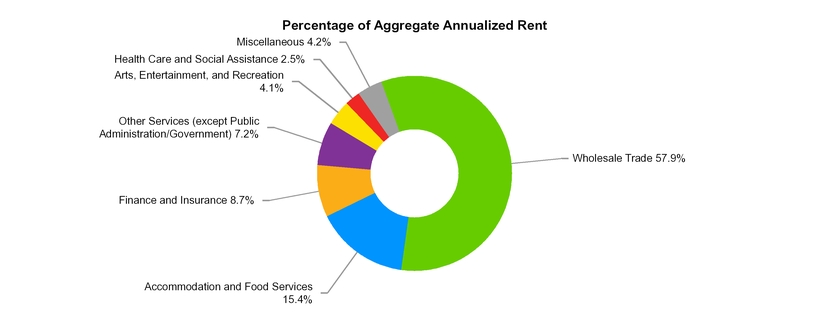

Industry Classification (NAICS) | Annualized Base Rental Revenue | | Percentage of Aggregate Annualized Rent | | Aggregate Rentable Square Feet | | Percentage of Aggregate Square Feet |

Retail: | | | | | | | |

Wholesale Trade | $ | 27,764,522 |

| | 57.89 | % | | 1,506,206 |

| | 71.26 | % |

Accommodation and Food Services | 7,375,128 |

| | 15.38 | % | | 223,634 |

| | 10.58 | % |

Finance and Insurance | 4,171,893 |

| | 8.70 | % | | 56,299 |

| | 2.66 | % |

Other Services (except Public Administration/Government) | 3,453,505 |

| | 7.20 | % | | 108,404 |

| | 5.13 | % |

Arts, Entertainment, and Recreation | 1,961,674 |

| | 4.09 | % | | 115,586 |

| | 5.47 | % |

Health Care and Social Assistance | 1,206,617 |

| | 2.52 | % | | 31,602 |

| | 1.49 | % |

Miscellaneous: | | | | | | | |

Manufacturing | 546,986 |

| | 1.14 | % | | 17,547 |

| | 0.83 | % |

Educational Services | 424,965 |

| | 0.89 | % | | 25,598 |

| | 1.21 | % |

Information (Broadcasting, Publishing, Telecommunications) | 354,305 |

| | 0.74 | % | | 8,347 |

| | 0.39 | % |

Other | 694,888 |

| | 1.45 | % | | 20,740 |

| | 0.98 | % |

Total | $ | 47,954,483 |

| | 100.00 | % | | 2,113,963 |

| | 100.00 | % |

|

| |

Lease Expirations | |

March 31, 2017 |

|

| | | | | | | | | | | | | | | | | | | | |

Year | | Number of Leases | | Rentable Square Feet | | Percent of Rentable Square Feet | | Annualized Rent (1) | | Average Rental Rate | | Percent of Annualized Rent (1) |

Office: | | | | | | | | | | | | |

2017 | | 43 |

| | 432,471 |

| | 11.96 | % | | $ | 17,210,006 |

| | $ | 39.79 |

| | 10.66 | % |

2018 | | 43 |

| | 225,386 |

| | 6.24 | % | | 9,384,424 |

| | 41.64 |

| | 5.81 | % |

2019 | | 59 |

| | 565,001 |

| | 15.63 | % | | 24,083,612 |

| | 42.63 |

| | 14.92 | % |

2020 | | 45 |

| | 398,525 |

| | 11.02 | % | | 19,308,917 |

| | 48.45 |

| | 11.96 | % |

2021 | | 58 |

| | 432,436 |

| | 11.96 | % | | 18,707,052 |

| | 43.26 |

| | 11.59 | % |

2022 and thereafter | | 167 |

| | 1,561,005 |

| | 43.19 | % | | 72,761,161 |

| | 46.61 |

| | 45.06 | % |

| | 415 |

| | 3,614,824 |

| | 100.00 | % | | $ | 161,455,172 |

| | 44.66 |

| | 100.00 | % |

Retail: | | | | | | | | | | | | |

2017 | | 19 |

| | 60,031 |

| | 2.83 | % | | $ | 1,940,345 |

| | $ | 32.32 |

| | 3.70 | % |

2018 | | 36 |

| | 334,268 |

| | 15.74 | % | | 4,828,539 |

| | 14.45 |

| | 9.22 | % |

2019 | | 33 |

| | 165,307 |

| | 7.78 | % | | 4,626,849 |

| | 27.99 |

| | 8.83 | % |

2020 | | 41 |

| | 437,339 |

| | 20.59 | % | | 7,831,476 |

| | 17.91 |

| | 14.95 | % |

2021 | | 23 |

| | 218,039 |

| | 10.26 | % | | 3,891,705 |

| | 17.85 |

| | 7.43 | % |

2022 and thereafter | | 137 |

| | 909,353 |

| | 42.80 | % | | 29,273,893 |

| | 32.19 |

| | 55.87 | % |

| | 289 |

| | 2,124,337 |

| | 100.00 | % | | $ | 52,392,807 |

| | 24.66 |

| | 100.00 | % |

Total: | | | | | | | | | | | | |

2017 | | 62 |

| | 492,502 |

| | 8.58 | % | | $ | 19,150,351 |

| | $ | 38.88 |

| | 8.96 | % |

2018 | | 79 |

| | 559,654 |

| | 9.75 | % | | 14,212,963 |

| | 25.40 |

| | 6.65 | % |

2019 | | 92 |

| | 730,308 |

| | 12.73 | % | | 28,710,461 |

| | 39.31 |

| | 13.43 | % |

2020 | | 86 |

| | 835,864 |

| | 14.56 | % | | 27,140,393 |

| | 32.47 |

| | 12.69 | % |

2021 | | 81 |

| | 650,475 |

| | 11.33 | % | | 22,598,757 |

| | 34.74 |

| | 10.57 | % |

2022 and thereafter | | 304 |

| | 2,470,358 |

| | 43.05 | % | | 102,035,054 |

| | 41.30 |

| | 47.70 | % |

| | 704 |

| | 5,739,161 |

| | 100.00 | % | | $ | 213,847,979 |

| | 37.26 |

| | 100.00 | % |

| | |

(1) Annualized Rent is equal to the rental rate effective at lease expiration (cash basis) multiplied by 12. | | |

|

| |

Schedule of Properties | |

March 31, 2017 |

|

| | | | | | | | | | | | |

PROPERTIES | | LOCATION | | YEAR ACQUIRED | | YEAR CONSTRUCTED | | NET RENTABLE SQUARE FEET | | Leased % |

Office Buildings | | | | | | | | | | |

515 King Street | | Alexandria, VA | | 1992 | | 1966 | | 75,000 |

| | 94 | % |

Courthouse Square | | Alexandria, VA | | 2000 | | 1979 | | 118,000 |

| | 94 | % |

Braddock Metro Center | | Alexandria, VA | | 2011 | | 1985 | | 348,000 |

| | 99 | % |

1600 Wilson Boulevard | | Arlington, VA | | 1997 | | 1973 | | 170,000 |

| | 100 | % |

Fairgate at Ballston | | Arlington, VA | | 2012 | | 1988 | | 143,000 |

| | 95 | % |

Monument II | | Herndon, VA | | 2007 | | 2000 | | 208,000 |

| | 84 | % |

925 Corporate Drive | | Stafford, VA | | 2010 | | 2007 | | 134,000 |

| | 73 | % |

1000 Corporate Drive | | Stafford, VA | | 2010 | | 2009 | | 137,000 |

| | 82 | % |

Silverline Center | | Tysons, VA | | 1997 | | 1972/1986/1999/2014 | | 544,000 |

| | 98 | % |

John Marshall II | | Tysons, VA | | 2011 | | 1996/2010 | | 223,000 |

| | 100 | % |

1901 Pennsylvania Avenue | | Washington, DC | | 1977 | | 1960 | | 102,000 |

| | 85 | % |

1220 19th Street | | Washington, DC | | 1995 | | 1976 | | 103,000 |

| | 99 | % |

1776 G Street | | Washington, DC | | 2003 | | 1979 | | 265,000 |

| | 94 | % |

2000 M Street | | Washington, DC | | 2007 | | 1971 | | 231,000 |

| | 100 | % |

2445 M Street | | Washington, DC | | 2008 | | 1986 | | 290,000 |

| | 100 | % |

1140 Connecticut Avenue | | Washington, DC | | 2011 | | 1966 | | 183,000 |

| | 90 | % |

1227 25th Street | | Washington, DC | | 2011 | | 1988 | | 136,000 |

| | 99 | % |

Army Navy Building | | Washington, DC | | 2014 | | 1912/1987 | | 109,000 |

| | 55 | % |

1775 Eye Street, NW | | Washington, DC | | 2014 | | 1964 | | 186,000 |

| | 100 | % |

Subtotal | | | | | | | | 3,705,000 |

| | 94 | % |

|

| |

Schedule of Properties (continued) | |

March 31, 2017 |

|

| | | | | | | | | | | | |

PROPERTIES | | LOCATION | | YEAR ACQUIRED | | YEAR CONSTRUCTED | | NET RENTABLE SQUARE FEET | | Leased % |

Retail Centers | | | | | | | | | | |

Bradlee Shopping Center | | Alexandria, VA | | 1984 | | 1955 | | 171,000 |

| | 99 | % |

Shoppes of Foxchase | | Alexandria, VA | | 1994 | | 1960/2006 | | 134,000 |

| | 100 | % |

800 S. Washington Street | | Alexandria, VA | | 1998/2003 | | 1955/1959 | | 46,000 |

| | 93 | % |

Concord Centre | | Springfield, VA | | 1973 | | 1960 | | 76,000 |

| | 72 | % |

Gateway Overlook | | Columbia, MD | | 2010 | | 2007 | | 220,000 |

| | 87 | % |

Frederick County Square | | Frederick, MD | | 1995 | | 1973 | | 227,000 |

| | 93 | % |

Frederick Crossing | | Frederick, MD | | 2005 | | 1999/2003 | | 295,000 |

| | 99 | % |

Centre at Hagerstown | | Hagerstown, MD | | 2002 | | 2000 | | 331,000 |

| | 95 | % |

Olney Village Center | | Olney, MD | | 2011 | | 1979/2003 | | 199,000 |

| | 98 | % |

Randolph Shopping Center | | Rockville, MD | | 2006 | | 1972 | | 82,000 |

| | 88 | % |

Montrose Shopping Center | | Rockville, MD | | 2006 | | 1970 | | 145,000 |

| | 98 | % |

Takoma Park | | Takoma Park, MD | | 1963 | | 1962 | | 51,000 |

| | 100 | % |

Westminster | | Westminster, MD | | 1972 | | 1969 | | 150,000 |

| | 98 | % |

Wheaton Park | | Wheaton, MD | | 1977 | | 1967 | | 74,000 |

| | 93 | % |

Chevy Chase Metro Plaza | | Washington, DC | | 1985 | | 1975 | | 50,000 |

| | 87 | % |

Spring Valley Village | | Washington, DC | | 2014 | | 1941/1950 | | 78,000 |

| | 81 | % |

Subtotal | | | | | | | | 2,329,000 |

| | 94 | % |

|

| |

Schedule of Properties (continued) | |

March 31, 2017 |

|

| | | | | | | | | | | | |

PROPERTIES | | LOCATION | | YEAR ACQUIRED | | YEAR CONSTRUCTED | | NET RENTABLE SQUARE FEET (1) | | Leased % |

Multifamily Buildings / # units | | | | | | | | | | |

Clayborne / 74 | | Alexandria, VA | | 2008 | | 2008 | | 60,000 |

| | 97 | % |

Riverside Apartments / 1,222 | | Alexandria, VA | | 2016 | | 1971 | | 1,266,000 |

| | 96 | % |

Park Adams / 200 | | Arlington, VA | | 1969 | | 1959 | | 173,000 |

| | 98 | % |

Bennett Park / 224 | | Arlington, VA | | 2007 | | 2007 | | 214,000 |

| | 97 | % |

The Paramount / 135 | | Arlington, VA | | 2013 | | 1984 | | 141,000 |

| | 96 | % |

The Maxwell / 163 | | Arlington, VA | | 2014 | | 2014 | | 139,000 |

| | 95 | % |

The Wellington / 711 | | Arlington, VA | | 2015 | | 1960 | | 842,000 |

| | 95 | % |

Roosevelt Towers / 191 | | Falls Church, VA | | 1965 | | 1964 | | 170,000 |

| | 96 | % |

The Ashby at McLean / 256 | | McLean, VA | | 1996 | | 1982 | | 274,000 |

| | 96 | % |

Bethesda Hill Apartments / 195 | | Bethesda, MD | | 1997 | | 1986 | | 225,000 |

| | 98 | % |

Walker House Apartments / 212 | | Gaithersburg, MD | | 1996 | | 1971/2003 | | 157,000 |

| | 98 | % |

3801 Connecticut Avenue / 307 | | Washington, DC | | 1963 | | 1951 | | 178,000 |

| | 95 | % |

Kenmore Apartments / 374 | | Washington, DC | | 2008 | | 1948 | | 268,000 |

| | 95 | % |

Yale West / 216 | | Washington, DC | | 2014 | | 2011 | | 238,000 |

| | 97 | % |

Subtotal (4,480 units) | | | | | | | | 4,345,000 |

| | 96 | % |

TOTAL | | | | | | | | 10,379,000 |

| | |

(1) Multifamily buildings are presented in gross square feet. | | |

|

| |

Supplemental Definitions | |

March 31, 2017 |

|

|

Adjusted EBITDA (a non-GAAP measure) is earnings attributable to the controlling interest before interest expense, taxes, depreciation, amortization, real estate impairment, casualty gain, gain on sale of real estate, gain/loss on extinguishment of debt, severance expense, relocation expense, acquisition and structuring expenses and gain/loss from non-disposal activities. |

Annualized base rent ("ABR") is calculated as monthly base rent (cash basis) per the lease, as of the reporting period, multiplied by 12. |

Debt service coverage ratio is computed by dividing earnings attributable to the controlling interest before interest expense, taxes, depreciation, amortization, real estate impairment, gain on sale of real estate, gain/loss on extinguishment of debt, severance expense, relocation expense, acquisition and structuring expenses and gain/loss from non-disposal activities by interest expense (including interest expense from discontinued operations) and principal amortization. |

Debt to total market capitalization is total debt divided by the sum of total debt plus the market value of shares outstanding at the end of the period. |

Earnings to fixed charges ratio is computed by dividing earnings attributable to the controlling interest by fixed charges. For this purpose, earnings consist of income from continuing operations (or net income if there are no discontinued operations) plus fixed charges, less capitalized interest. Fixed charges consist of interest expense (excluding interest expense from discontinued operations), including amortized costs of debt issuance, plus interest costs capitalized. |

Economic occupancy is calculated as actual real estate rental revenue recognized for the period indicated as a percentage of gross potential real estate rental revenue for that period. We determine gross potential real estate rental revenue by valuing occupied units or square footage at contract rates and vacant units or square footage at market rates for comparable properties. We do not consider percentage rents and expense reimbursements in computing economic occupancy percentages. |

Ending Occupancy is calculated as occupied square footage as a percentage of total square footage as of the last day of that period. Multifamily unit basis ending occupancy is calculated as occupied units as a percentage of total units as of the last day of that period. |

NAREIT Funds from operations ("NAREIT FFO") is defined by National Association of Real Estate Investment Trusts, Inc. (“NAREIT”) in an April, 2002 White Paper as net income (computed in accordance with generally accepted accounting principles (“GAAP”) excluding gains (or losses) associated with sales of property, impairment of depreciable real estate and real estate depreciation and amortization. We consider NAREIT FFO to be a standard supplemental measure for equity real estate investment trusts (“REITs”) because it facilitates an understanding of the operating performance of our properties without giving effect to real estate depreciation and amortization, which historically assumes that the value of real estate assets diminishes predictably over time. Since real estate values have instead historically risen or fallen with market conditions, we believe that NAREIT FFO more accurately provides investors an indication of our ability to incur and service debt, make capital expenditures and fund other needs. NAREIT FFO is a non-GAAP measure. |

Core Funds From Operations ("Core FFO") is calculated by adjusting NAREIT FFO for the following items (which we believe are not indicative of the performance of Washington REIT’s operating portfolio and affect the comparative measurement of Washington REIT’s operating performance over time): (1) gains or losses on extinguishment of debt, (2) expenses related to acquisition and structuring activities, (3) executive transition costs and severance expense related to corporate reorganization and related to executive retirements or resignations, (4) property impairments, casualty gains and losses, and gains or losses on sale not already excluded from NAREIT FFO, as appropriate, and (5) relocation expense. These items can vary greatly from period to period, depending upon the volume of our acquisition activity and debt retirements, among other factors. We believe that by excluding these items, Core FFO serves as a useful, supplementary measure of Washington REIT’s ability to incur and service debt, and distribute dividends to its shareholders. Core FFO is a non-GAAP and non-standardized measure, and may be calculated differently by other REITs. |

Funds Available for Distribution ("FAD") is calculated by subtracting from NAREIT FFO (1) recurring expenditures, tenant improvements and leasing costs, that are capitalized and amortized and are necessary to maintain our properties and revenue stream (excluding items contemplated prior to acquisition or associated with development / redevelopment of a property) and (2) straight line rents, then adding (3) non-real estate depreciation and amortization, (4) non-cash fair value interest expense and (5) amortization of restricted share compensation, then adding or subtracting the (6) amortization of lease intangibles, (7) real estate impairment and (8) non-cash gain/loss on extinguishment of debt, as appropriate. FAD is included herein, because we consider it to be a performance measure of a REIT’s ability to incur and service debt and to distribute dividends to its shareholders. FAD is a non-GAAP and non-standardized measure, and may be calculated differently by other REITs. |